Message Board")

Post by tomsylver on Nov 26, 2018 23:01:14 GMT

Portola Pharmaceuticals: Buy, Sell Or Hold?

Nov. 26, 2018 11:45 AM ET|

Bret Jensen

Specializing in biotech stocks, Small Caps, managing optimized portfolios

Marketplace

The Biotech Forum

Summary

* Today, we revisit Portola Pharmaceuticals.

* After a big slide in 2018, the shares seem to be stabilizing recently after third quarter results and a management change.

* We present an updated investment case around Portfola in the paragraphs below.

"I did not want to be taken for a fool - the typical French reason for performing the worst of deeds without remorse." - Jules Barbey d'Aurevilly, The Crimson Curtain

The market just had its worst Thanksgiving week as far as performance since 2011. All the major indices lost at least 3.5% on the week. This continues to be a putrid quarter for investors.

High beta areas of like biotech, small caps and commodities have been crushed so far this quarter while the FAANG stocks are in bear market territory now as well.

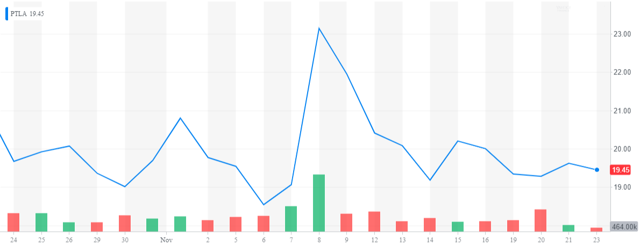

The SPDR Biotech ETF (XBI) is down almost 25% from its highs in early September. One small biotech stock that has held up quite well in this onslaught is Portfola Pharmaceuticals (PTLA) whose stock is trading right near the levels of once month ago.

Company Overview

The most important of these is Andexxa. This compound is targeted at being a "universal antidote" for the new breed of anticoagulants like Eliquis. This is something the industry has desperately needed for some time, as more than 80,000 individuals end up in the emergency room annually in the United States due to negative reactions to these medications, many of them life threatening. Andexxa was just approved in May of this year and is just being rolled out. The second generation Andexxa should be approved at yearend. The first generation is only being marketed to select hospitals. Approval of the second generation Andexxa will kick manufacturing and marketing of Andexxa into overdrive.

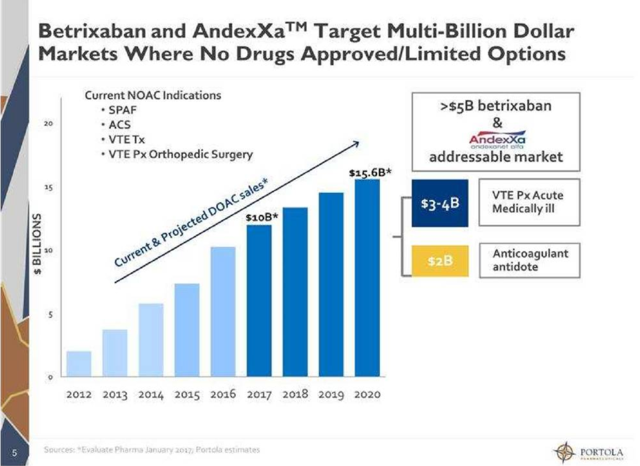

The other compound in Portola's product portfolio is Bevyxxa or betrixaban which was approved for Venous thromboembolism (VTE) Prevention in the early summer of 2017. To be more specific, Bevyxxa is the only FDA approved drug for VTE in adult patients hospitalized for an acute medical illness who are at risk for thromboembolic complication due to moderate or severe restricted mobility and other risk factors for VTE.

Source: Investor Presentation.

Third-Quarter Results:

The company posted a loss of $1.08 a share on revenues of just under $15 million in revenues. Both results were significantly better than expected. However, this appears to be a function of the $7 million in collaboration and license revenues Portola booked in the third quarter. Bevyxxa sales were flat at just over $500,000 while Andexxa sales came in at $7.7 million. This was more than triple the $2.2 million of sales Andexxa booked in the second quarter.

Analyst Commentary and Balance Sheet:

Verdict:

In the third quarter of this year, the company appointed Scott Garland as its CEO. Mr. Garland hails from Relypsa which was sold for sizable premium to Galencia for just over $1.5 billion in the summer of 2016. I think this appointment increases the chances this much speculated buyout target goes down that path eventually.

Option Strategy:

Another way to add exposure to this name currently given the dismal sentiment on the small cap market is via a Buy-Write order. Using the June $20 call strikes, fashion a Buy-Write order with a net debit in the $15.40 to $15.60 range (net stock price - option premium). This mitigates some downside risk and sets up a more than solid potential return for its approximate eight month hold period. Option liquidity is decent in this strike price.

"Good God, if our civilization were to sober up for a couple of days, it'd die of remorse on the third." - Malcolm Lowry, Under the Volcano

Bret Jensen is the Founder and author of articles on The Biotech Forum, The Busted IPO Forum, and The Insiders Forum. To receive these articles as published on Seeking Alpha, just click the appropriate link and hit the orange follow button.

Disclosure: I am/we are long PTLA,XBI.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Nov. 26, 2018 11:45 AM ET|

Bret Jensen

Specializing in biotech stocks, Small Caps, managing optimized portfolios

Marketplace

The Biotech Forum

Summary

* Today, we revisit Portola Pharmaceuticals.

* After a big slide in 2018, the shares seem to be stabilizing recently after third quarter results and a management change.

* We present an updated investment case around Portfola in the paragraphs below.

"I did not want to be taken for a fool - the typical French reason for performing the worst of deeds without remorse." - Jules Barbey d'Aurevilly, The Crimson Curtain

The market just had its worst Thanksgiving week as far as performance since 2011. All the major indices lost at least 3.5% on the week. This continues to be a putrid quarter for investors.

High beta areas of like biotech, small caps and commodities have been crushed so far this quarter while the FAANG stocks are in bear market territory now as well.

To be fair, the shares had already been more than cut in half in 2018 before the carnage in equities started this fourth quarter.

However, the prospects for this beaten down story had also been bolstered by decent third quarter results and a recent management change. We take a look at both in the paragraphs below.

Portfola Pharmaceuticals is based in Northern California. The shares currently trade at approximately $19.50 a share and have a $1.3 billion market capitalization. The company has two approved products recently approved for the market.

The most important of these is Andexxa. This compound is targeted at being a "universal antidote" for the new breed of anticoagulants like Eliquis. This is something the industry has desperately needed for some time, as more than 80,000 individuals end up in the emergency room annually in the United States due to negative reactions to these medications, many of them life threatening. Andexxa was just approved in May of this year and is just being rolled out. The second generation Andexxa should be approved at yearend. The first generation is only being marketed to select hospitals. Approval of the second generation Andexxa will kick manufacturing and marketing of Andexxa into overdrive.

Portfola's two approved drugs are targeting significant markets. The company has another promising compound Cerdulatinib in development. Cerdulatinib has been granted the Orphan Drug Designation by the FDA for the treatment of peripheral T-cell lymphoma. A pivotal trial for this condition should kick off in the first quarter of next year. Updated Phase 2 data for the treatment of refractory non-Hodgkin lymphoma and chronic lymphocytic leukemia - cancer will be presented at the big American Society of Hematology or ASH conference on December 3rd.

The company posted a loss of $1.08 a share on revenues of just under $15 million in revenues. Both results were significantly better than expected. However, this appears to be a function of the $7 million in collaboration and license revenues Portola booked in the third quarter. Bevyxxa sales were flat at just over $500,000 while Andexxa sales came in at $7.7 million. This was more than triple the $2.2 million of sales Andexxa booked in the second quarter.

General and administrative expenses for the third quarter of 2018 were $38.8 million as Portola ramped up its sales force. Research and development expenses were $40.2 million in the quarter, approximately $12 million of this was for the second generation of Andexxa. Approval by year end will support a much broader launch as well as faster sales growth and also cause this expense to be dissipated in the quarters ahead.

While the initial reaction of the market to third quarter results boosted the stock of Portola, analyst commentary was not as enthusiastic as one might think. Oppenheimer and Credit Suisse both lower their price targets to $30.00 a share while Cowen & Co. lowered their price target to $45 (from $50 previously). Both Cowen and Oppenheimer maintained their Buy ratings on PTLA while Credit Suisse remains a Hold on the stock. The company ended the third quarter with approximately $380 million in cash and marketable securities on the books.

In the third quarter of this year, the company appointed Scott Garland as its CEO. Mr. Garland hails from Relypsa which was sold for sizable premium to Galencia for just over $1.5 billion in the summer of 2016. I think this appointment increases the chances this much speculated buyout target goes down that path eventually.

In the meantime, the company is advancing its pipeline and aiming at large potential markets. One overhang is Portola will probably have to do a capital raise over the next couple of quarters even as R&D expenses fall and revenues ramp up in the quarters ahead. However, given the decline in the stock in 2018, that could very well be priced into the shares. The stock seems to have found a floor and the long term risk/reward profile of Portola seems favorable despite the dismal current market environment.

Another way to add exposure to this name currently given the dismal sentiment on the small cap market is via a Buy-Write order. Using the June $20 call strikes, fashion a Buy-Write order with a net debit in the $15.40 to $15.60 range (net stock price - option premium). This mitigates some downside risk and sets up a more than solid potential return for its approximate eight month hold period. Option liquidity is decent in this strike price.

"Good God, if our civilization were to sober up for a couple of days, it'd die of remorse on the third." - Malcolm Lowry, Under the Volcano

Bret Jensen is the Founder and author of articles on The Biotech Forum, The Busted IPO Forum, and The Insiders Forum. To receive these articles as published on Seeking Alpha, just click the appropriate link and hit the orange follow button.

Disclosure: I am/we are long PTLA,XBI.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.