Message Board")

Seeking Alpha Article Carnage In Junior Biotechs by DoctorRx

Sept 30, 2015 17:27:03 GMT

thought013 likes this

Post by Uncle on Sept 30, 2015 17:27:03 GMT

More Carnage In Junior Biotechs: General Comments With Focus On Opko And Acceleron

DoctoRx

SeekingAlpha

Sep. 30, 2015 12:35 PM ET | About: Acceleron Pharma Inc. (XLRN), OPK, Includes: AET, AMGN, CELG, GILD, HYG, IBB, IEP, MRK, PFE, SPY, TSRO, UNH, VRX, XBI

Disclosure: I am/we are long OPK,XLRN,GILD,AMGN. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Summary

Background

Smaller biotechs (NYSEARCA:XBI) have entered a vortex, underperforming their large cap peers (NASDAQ:IBB) Tuesday. After having matters all their own way for several years, and then with too many marginal IPOs being brought forth (tech, biotech and otherwise), the group has been hit first by a political candidate's tweet and speech and then a request from Congress that Valeant (NYSE:VRX), a Canadian company that has not been shy about raising drug prices, appear before it. That request likely contributed to this week's further price declines on pharmaceutical and biotech stocks.

Unsurprisingly, a set of warnings from the financial media began to be heard that the end of the pharma/biotech bull market may be nigh.

For example, on Monday, CNBC ran a video titled Step away from biotechs, let dust settle: Pro. Tuesday, CNBC ran a video, Here's the big problem with biotech: Trader.

Now they tell us.

Also on Tuesday, the media highlighted Carl Icahn prophesying a general sort of doom. Though maybe the drop in the share price of Icahn Holdings (NASDAQ:IEP) from $103 to $66 over the past 12 months has depressed him.

A common view of biotechs, especially junior biotechs, comes from a current blog which reads in part:

The biotech party

Here's the weekly StockCharts view (not shown: ed.) of the exchange-traded fund for the S&P Biotech Index . The heart of the bubble, it has the classic parabolic rise of an investment mania. Now down almost 30% from its July record high. Propelled by vapors and dreams, we need not consult Nostradamus to guess at what comes next. For details see Don't ask if there's a biotech bubble. Ask why we have another bubble.

How accurate is the view that share appreciation of IBB stalwarts such as Gilead (NASDAQ:GILD), Celgene (NASDAQ:CELG), Amgen (NASDAQ:AMGN), etc. have been propelled by "vapors and dreams" rather than actual sales and EPS growth? Not very.

This sort of thinking is all over, and it can temporarily create its own reality. It is as if intelligent people have forgotten the difference between a boom and a bubble. Yes, we all know that the Fed printed a lot of excess money. But some companies and industries have done poorly, and their stocks have been punished. Others have done well, and their stocks have risen.

In other words, a bear market psychology appears to have taken over biotech stock pricing, which as I and others pointed out some months ago, had been too strong relative to the market (NYSEARCA:SPY) for too long and was due for a reset.

Maybe the whole negativity trend has gone a bit too far. Even an M.D. who sought out analysis for a profession, Dr. Schoenebaum of ISI, may have drunk deeply from the bearish cup. Just think how far psychology has changed when Barron's blog Tuesday was titled Gilead Sciences: How Bad Can It Get?. From that blog:

Evercore ISI's Mark Schoenebaum decided to stress test his models for Gilead Sciences (GILD), Biogen (BIIB), Amgen (AMGN) and Celgene (CELG), among others, to see what would happen in a worst case pricing scenario. Here's what he did:

1. taken our base case discounted cash flows and cut base US business (i.e. non-pipeline) revenue by 5%-20% starting in 2018 (starting at 5% in 2018, ramping to 20% over 4 years) to reflect general "pricing risk."

2. Cut all my pipeline estimates by 20%.

3. Assumed a -1% terminal growth rates (which is down from 0% or +1% in most of our models)...

The results? Gilead could fall as low as $77...

Here's what stands out to me - that GILD's terminal growth rate is assumed to be around zero. Anyone can assume any price cuts they want for any industry as an exercise, but how does biotech/biopharma end up with a terminal growth rate (future growth only five years, apparently) of about zero?

Well, Dr. Schoenebaum and DoctoRx appear to differ on that point. I'm more optimistic for the industry as being likely to experience secular growth.

Junior biotechs amplify the mood of the marginal investor. So if the terminal growth rate for the titans of the biotech industry is around zero, what hope is there for money-losing juniors?

The bearish/cautious views of Dr. Schoenebaum, Carl Icahn, and others are consistent with the implications of a behavioral indicator I have followed since it was introduced in the early part of this century, the Smith Barney "Other P/E" (Panic/Euphoria) indicator. When I a client of Smith Barney, I saw it work pretty well in real time. Now it's tough to get hold of, but this past Sunday I found a good technically-oriented blog that had a current version of it. It looks as though investors are deep in panic mode. In the past, this has been followed by a nicely higher stock market 12 months later. From The Fat Pitch:

While it's a little difficult to see (click to enlarge), the light blue line has just collapsed to deep panic levels. There are certainly no guarantees about the reliability of this indicator, but it fits the theme I'm seeing right now.

This chart was seen on Sunday, so it may or may not have included Friday's big down day, and it definitely did not include Monday's heavy selling pressure. So, it's possible that this indicator may show as much panic, or even a little more, than it measured at the bottom(s) in 2008-9.

The correlation of the SPY with these behavioral analyses may or may not continue to "work," and for sure they may have nothing to do with the action of any one specific sector.

Introduction - follow the cash burn and junk bond yields

One of the fundamental problems with junior biotechs is their need for new cash. Few new products on the market turn cash flow positive early on, so financing is needed for some time after a junior biotech succeeds in bringing a product to market. Any "risk off" episode with lower stock prices, rising sub-investment grade bond yields (i.e. declining prices of "junk" bonds) raises a company's financing costs, forces it to do some combination of additional shareholder dilution (including that of the insiders) and/or reduction of growth plans, and may negatively influence employee work effort.

In contrast, highly profitable majors such as Gilead can gain from these episodes. IPOs have already stopped. It may be easier to purchase a private company than a public one; and less expensive as well.

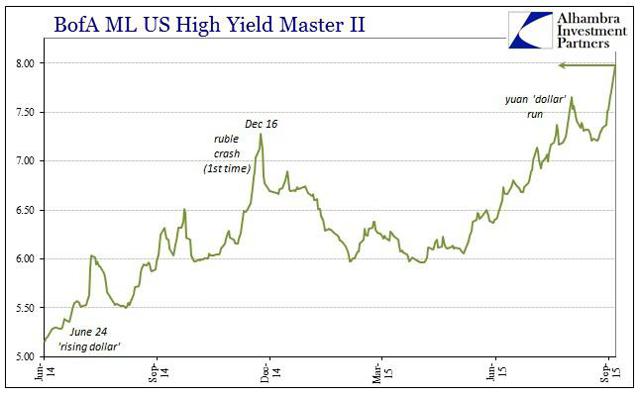

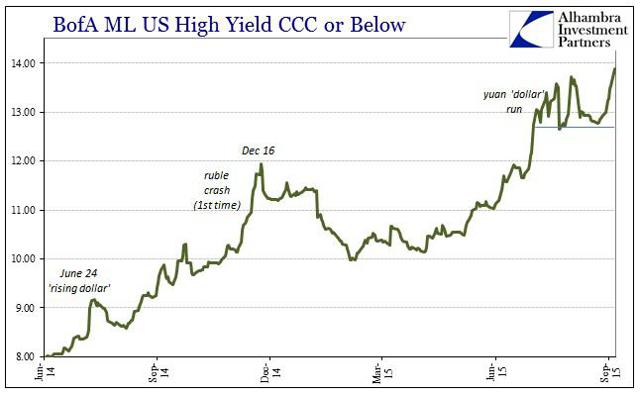

For this reason, the following charts of high-yield bonds has finally begun to correlate with the price action of the cash-burning junior biotechs. First, a large high-yield bond ETF (NYSEARCA:HYG):

This is pretty dismal. It's no surprise that directionally, XBI has finally begun moving in the same downward direction.

The credit spreads versus Treasury yields are also blowing out;

So, putting things together, it's no surprise that the double whammy of politically-induced (and sudden) worries about pricing and a major bear market in junk bonds has changed Mr. Market's method of valuing an unchanged set of unprofitable companies. Cost of and availability of capital have been worsening at the same time as a more cautious view of future pricing flexibility has begun to take hold.

Thinking through what a junior biotech stock represents

Yes, investing in a junior biotech is a form of gambling. However, I try to be like the young Bill Gross, who before building PIMCO up was a card-counter at Vegas and beat the house. So long as one is not investing in an extremely early-stage company (see my criticism of inappropriate IPOs above), here is what I look for in a company.

My bias is to think of this sort of investment as if it were an intermediate-term zero coupon bond, though with greater liquidity assuming the company is public. As with a zero, there is no possibility of current income. At some point, the company will either be generating sales/profits, or not. If not, the investment is a loser, though maybe not a complete wipe-out. If the company has succeeded in reaching a certain level, then unlike the zero coupon bond, where the upside is capped at par, the valuation of the stock has an infinite range. So it's my job as an investor to make projections based on known products that are planned to operate in established market niches (specific diseases, in most cases). And of course, the yields available on other sub-investment grade alternatives, such as junk bonds, must be considered. We all have our own hurdle rates for that sort of metric.

However, unlike Dr. Schoenebaum, I do not assume a terminal growth rate of zero for any biotech, large or small. I assume that the field will be viewed as a growth field 5-10 years from now.

Now, the "thing" about a zero coupon bond is that it either pays off or not. How it trades is not the point. The same is true of junior biotech stocks. Traders whip them around. As discussed above, sentiment swings manifest themselves most strongly not in the major biotechs , but in the juniors that have no discernible, measurable value as operating companies.

So, if sentiment gets very bearish, the greatest upside should come from the juniors if their stocks have been battered.

The other question that affects the juniors even more than the major biotechs is whether the government is really going to harm the industry. Are there really excess profits in biotech, or are there just a few sharpies dealing with old, non-biotech drugs, such as the recent Times article pointed to?

How likely is new Federal legislation that would be directly adverse to biotechs?

I believe that it's unlikely.

The pharmaceutical industry in general and biotech in specific provide a growing number of high-paying jobs that are located in the United States. Biotech companies contribute very positively to the country's balance of trade. This is a tough industry to deliberately hamper.

Recent history suggests biotech investors need not fear; any future legislative damage to the industry may already have either been incorporated or over-incorporated into stock prices.

To wit:

Even with a filibuster-proof majority in the Senate, the Democrats did not try to lay a glove on Big Pharma in the "Obamacare" legislation.

Before that, in 1994, some members of Big Pharma, including (if memory serves) Merck (NYSE:MRK) - the most influential pharma company at the time - were sympathetic to President Clinton's health care reform initiative. Then Hillary Clinton gave what I recall the New York Times referring to as the most bare-knuckled attack speech given by a First Lady in memory. That attack against the pharmaceutical industry angered Merck and may have doomed "Clintoncare."

It is not forgotten by today's politicians that the year of the Clintoncare failed legislation and the year Obamacare passed turned out to be mid-term election years that were historic disasters for the President's party.

So, from a brute political standpoint, there are easier industries to go after.

Also, politicians are people too. And when all is said and done, they want the best medicines for themselves and their families. They want breakthrough medicines as much as we all do.

As it happens, the Medicare Part D system does lead to price pressures on manufacturers, as providers set up their preferred drug networks. This battle was fought a decade ago, was not a point of controversy during the work-up of the Obamacare legislation, and would be difficult to alter via new legislation.

If constitutional, a narrow bit of legislation that addresses sudden, huge jumps in single-source drug prices might be achieved. That might not be an easy task, though.

Of course, anything can happen, but this recent stuff strikes me as typical political theater.

A word about XBI

I have often mentioned XBI, the SPDR S&P Biotech ETF, as a placeholder or example for junior biotechs. It's really not a pure junior biotech ETF. GILD is in it, and some non-biotech stocks are in it. But it will do as a proxy.

However, I am not bullish on XBI; that general feeling ended this summer, as has amply been described in several articles back then. Since feeling that the biotechs were primed for a summer fall, I have believed that specific company analysis going to prevail. So far, that has not worked, but we are still in the maelstrom. Specifically, they say that few battle plans survive contact with the enemy, and in this case, the pricing issue was not in my rational expectations playbook for the biotech sector. So be it. If politicians want to promise healthcare for the masses, they know that it's costly.

What many of them also know is that technology is deflationary when properly defined, and that applies to biotechnology as well. As an example and as a way of segueing to specific company discussion, let's take Opko (NYSE:OPK).

How Opko's product line exemplifies the difficulties facing would-be pharmaceutical cost controllers

OPK is the third major pharma vehicle for Dr. Phillip Frost, a 78-year old dermatologist. The first, Key Pharmaceuticals, was a pioneer in controlled-release drugs, and was sold in the mid-1980's to Schering-Plough.

OPK has been utterly crushed in the recent deluge, with Dr. Frost buying blocks of the stock on the way down. Note, while OPK is often considered a biotech, it's much more diversified than that. Its diversification, which includes a reference lab (via recent acquisition) and a diagnostic test for prostate cancer, makes it a good example of the difficulty politicians will have trying to bring down pharmaceutical prices.

First up, OPK acquired rolapitant, which had to be divested when MRK and Schering-Plough merged. The drug was not right for OPK to develop, and it found Tesaro (NASDAQ:TSRO), a young pharma company focusing on oncology, to take it through FDA approval. Rolapitant happily received FDA marketing approval as Varubi for prevention of chemo-induced nausea/vomiting a few weeks ago. It has generic competition in its class. In order for this drug to bring its benefits to patients, it has to have a long patent life and pricing flexibility. OPK had to have the incentive to buy the drug, and TSRO had to have the incentive to develop it with enough ROIC for OPK to receive royalty payments. Absent these conditions, it's quite possible that rolapitant never would have come to market. Eventually, of course, it will go generic and society will have permanent low-cost benefit from it. This sounds reasonable to me, not requiring new legislation.

Next up for OPK, Rayaldee. This is awaiting FDA approval. Rayaldee is said to be an improved formulation of (slightly simplifying for lay readers) vitamin D, with special benefits for many patients with kidney disease. Assuming this is an improved product that can successfully compete against the wide variety of vitamin D-like drugs already available, then Rayaldee will also return its profits into OPK and from OPK into the economy as a whole, then go generic and be available inexpensively to all who need it. Rejiggering the patent or pricing scheme to save a little money up front for payors could easily lead future products such as Rayaldee to simply not be developed.

Moving on to the last example, OPK is utilizing technology it acquired to develop a long-acting growth hormone. It has attracted Pfizer (NYSE:PFE) as its partner here. Instead of daily administration for today's growth hormone therapies, including PFE's own brand, the OPK version is given only once a week, also by subcutaneous injection. Presumably this will improve patient adherence and can cut drug acquisition cost by the payor, as well as greatly reducing the use of needles etc.

When I think of the chain of development of the controlled-release technology in this product, the ups and downs of the companies involved, and the commercial failure of at least one prior controlled-release growth hormone product despite FDA approval, I think that only an attractive patent and regulatory regime would attract further innovation in this product category. What would happen if the US made matters materially tougher for pharma companies would in my view be the off-shoring of a progressively greater percentage of product and pharma technology development - and soon.

So I just don't see it really happening, at least to any greater extent than the stocks have already priced in.

The above is not anything close to a full analysis of OPK, which has more going on than these drugs, including even more innovative products in earlier stages of development, as well as its large diagnostics business.

The point of discussing the three products discussed above is that they represent a spectrum of improved (or, allegedly improved) formulations or new chemical entities without which the world would keep spinning. Some or all of these products, which will become cheap at some point assuming they prove useful, may well never have come to public awareness. The absence of their development, at least their development by a US company in the US, would not be known. The lack of their development under different patent and pricing conditions fits with words from Bastiat:

In the economic sphere an act, a habit, an institution, a law produces not only one effect, but a series of effects. Of these effects, the first alone is immediate; it appears simultaneously with its cause; it is seen. The other effects emerge only subsequently; they are not seen; we are fortunate if we foresee them.

The benefits of price controls harsh enough to "move the needle" would be seen at once, and might even win an election. But I'm willing to invest on a scenario in which pharma and biotech innovation continues to be encouraged right here in the United States.

A more classic biotech junior is discussed next.

A (very) brief review of the biotech process: focus on Acceleron (NASDAQ:XLRN)

A Celgene affiliated-company, this company has been around many years. After years of effort, and extensive assistance from CELG (the top-rated pharma partnering company), one of its products is finally ready to enter Phase 3 testing for orphan diseases. This protein, luspatercept, is hoped to come to market for beta-thalassemia and myelodysplastic syndrome, two different anemias. A related drug, sotatercept, was recently disclosed by the CEO to be a "maybe" about advancement to Phase 3 for complications of renal failure with anemia. This "maybe" could be the cause of the stock sinking to an interim new closing low this week. XLRN is down from the high $50s, a price reached in the winter of 2014. Its action shows that the sector is not monolithic.

The stock has come down to earth. It could definitely go much lower, but I think it could also generate much larger profits over time than its market cap suggests, adjusted for an appropriate discount rate.

After all these years of research, XLRN is a $25 stock with an ex-cash market cap around $700 million. In several years, I think that its royalties from CELG could be well over $100 million per year and could grow from there, perhaps to hundreds of millions of dollars per year (it's really too early to get specific, though).

Luspatercept might fail in Phase 3 or surprise CELG and get approved but not succeed in the marketplace.

Given a growing pipeline, XLRN looks interesting to me.

At the least, if luspatercept comes to market, the current patent, regulatory and payment system will have brought a useful and even breakthrough medicine to benefit a group of people who through no fault of their own are suffering. Not only have many years of research, invention, blind alleys, etc. gone into the development of this one candidate, there still is nothing approaching certainty that anyone will ultimately make a dime off of it.

Whatever profits XLRN eventually generates, many years after embarking on its quest to make money the right way, by improving the world as we know it, will be justly earned. There will be no profiteering. I think Mr. Market knows this. (I bought more XLRN on this dip/crash, having sold most of my shares in the recent "rip" to $35.)

XLRN is a classic example of the risks and rewards of investing in a start-up wherein the only certainty is years of cash burn. This sort of investing is clearly not for all investors. It's my view, though, that it has led to robust improvements in pharmaceutical development that would not have occurred had the old way of Big Pharma driving almost all product development continued.

My expectation is that the US will continue to encourage this sort of risk-taking, for the greater good.

Summary and concluding thoughts - why pick on biotech?

In contrast to research-based pharmaceutical companies in general and biotechnology companies in specific, let's take a look at the tangible assets found in health insurers such as Aetna (NYSE:AET) and UnitedHealth (NYSE:UNH). But don't look too hard; summing up their tangible assets gives a negative number - less than XLRN.

What have these acquisitive giants actually contributed to human wellbeing to merit the future profits that are embodied in their stock market valuations? What have they invented? What risks have they taken?

Might America go the route of many other developed countries and remove all profits from the insurance business?

Wouldn't that actually save a lot of money?

The example of the refusal of the insurers to actually pay for hepatitis C cures in all patients with a prescription from a physician who wants to cure that patient suggests to me that these are not risk-based companies the way true insurers are. Rather, perhaps they are more like government-sponsored enterprises that make their money rationing care.

If Congress and the next President want to pick on a healthcare industry to save money, the health insurance industry is my candidate. Back in 2013, I correctly picked AET as a stock that could double - and it did. I'm out of it now, and for the robots that scan these articles to track the investment calls made by authors, I'm no longer bullish on AET.

We could be on the verge of a major wipe-out in the stock market. Those who "panicked" (i.e. sold) recently may have panicked correctly. Today could be like 1929, or worse. Or it could be 1998 or 2011, with months or years of upside price action and a growing economy ahead of us following a few months of downside price action.

As I see it, the junior biotech sector is one of the most dynamic of all parts of the US and global economy. It has been dumped on by political rhetoric, and the bears are growling loudly and publicly, both on the sector and the market. But their success comes from innovation, and only requires pricing within settled parameters to drive further investment. Absent that investment, progress in the sector will increasingly come from ex-US venues.

In addition, it's possible that the junk bond sector is seeing or has seen the worst of its troubles (that's not a prediction), especially the non-energy, non-mining/mineral high-yield bonds.

Thus both sentiment and one relevant fundamental might turn around, and perhaps soon.

After all, the world turns every 24 hours, and headlines change that fast as well. With that daily change can come, sooner or later, the realization that in the generally-mature US economy, it's pretty much only "tech" companies, plus "tech" as in biotech and related fields, that are true growth drivers right now. There's just not all that much innovation on a large scale elsewhere that I see as an investor who's always looking for new places to invest.

Thus I see the current bear market in junior biotechs as presenting interesting opportunities for new risk-oriented money that has a patient approach - though there may be great trading opportunities along the way. As stated, though, I have no special investing views on XBI or other small cap-oriented biotech funds; my analysis is of individual companies.

Note that risk is high, though, for all biotech stocks, and is magnified in the juniors. Trying to catch the falling knife can lead to a bloody outcome.

In a follow-up article planned to be completed and submitted to the editors soon, I'll present updates on a number of other junior biotechs.

Additional disclosure: Not investment advice. I am not an investment adviser.

DoctoRx

SeekingAlpha

Sep. 30, 2015 12:35 PM ET | About: Acceleron Pharma Inc. (XLRN), OPK, Includes: AET, AMGN, CELG, GILD, HYG, IBB, IEP, MRK, PFE, SPY, TSRO, UNH, VRX, XBI

Disclosure: I am/we are long OPK,XLRN,GILD,AMGN. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Summary

- The carnage in junior biotechs continued Monday and Tuesday, with more news out of politicians harming sentiment.

- While there is clearly substantial downside action possible from here, evidence is mounting that perhaps the bears are growling too loudly.

- Commentary on factors moving the junior biotech stocks is presented.

- Both Opko and Acceleron are discussed, as well, to illustrate the points made in the first parts of the article.

Background

Smaller biotechs (NYSEARCA:XBI) have entered a vortex, underperforming their large cap peers (NASDAQ:IBB) Tuesday. After having matters all their own way for several years, and then with too many marginal IPOs being brought forth (tech, biotech and otherwise), the group has been hit first by a political candidate's tweet and speech and then a request from Congress that Valeant (NYSE:VRX), a Canadian company that has not been shy about raising drug prices, appear before it. That request likely contributed to this week's further price declines on pharmaceutical and biotech stocks.

Unsurprisingly, a set of warnings from the financial media began to be heard that the end of the pharma/biotech bull market may be nigh.

For example, on Monday, CNBC ran a video titled Step away from biotechs, let dust settle: Pro. Tuesday, CNBC ran a video, Here's the big problem with biotech: Trader.

Now they tell us.

Also on Tuesday, the media highlighted Carl Icahn prophesying a general sort of doom. Though maybe the drop in the share price of Icahn Holdings (NASDAQ:IEP) from $103 to $66 over the past 12 months has depressed him.

A common view of biotechs, especially junior biotechs, comes from a current blog which reads in part:

The biotech party

Here's the weekly StockCharts view (not shown: ed.) of the exchange-traded fund for the S&P Biotech Index . The heart of the bubble, it has the classic parabolic rise of an investment mania. Now down almost 30% from its July record high. Propelled by vapors and dreams, we need not consult Nostradamus to guess at what comes next. For details see Don't ask if there's a biotech bubble. Ask why we have another bubble.

How accurate is the view that share appreciation of IBB stalwarts such as Gilead (NASDAQ:GILD), Celgene (NASDAQ:CELG), Amgen (NASDAQ:AMGN), etc. have been propelled by "vapors and dreams" rather than actual sales and EPS growth? Not very.

This sort of thinking is all over, and it can temporarily create its own reality. It is as if intelligent people have forgotten the difference between a boom and a bubble. Yes, we all know that the Fed printed a lot of excess money. But some companies and industries have done poorly, and their stocks have been punished. Others have done well, and their stocks have risen.

In other words, a bear market psychology appears to have taken over biotech stock pricing, which as I and others pointed out some months ago, had been too strong relative to the market (NYSEARCA:SPY) for too long and was due for a reset.

Maybe the whole negativity trend has gone a bit too far. Even an M.D. who sought out analysis for a profession, Dr. Schoenebaum of ISI, may have drunk deeply from the bearish cup. Just think how far psychology has changed when Barron's blog Tuesday was titled Gilead Sciences: How Bad Can It Get?. From that blog:

Evercore ISI's Mark Schoenebaum decided to stress test his models for Gilead Sciences (GILD), Biogen (BIIB), Amgen (AMGN) and Celgene (CELG), among others, to see what would happen in a worst case pricing scenario. Here's what he did:

1. taken our base case discounted cash flows and cut base US business (i.e. non-pipeline) revenue by 5%-20% starting in 2018 (starting at 5% in 2018, ramping to 20% over 4 years) to reflect general "pricing risk."

2. Cut all my pipeline estimates by 20%.

3. Assumed a -1% terminal growth rates (which is down from 0% or +1% in most of our models)...

The results? Gilead could fall as low as $77...

Here's what stands out to me - that GILD's terminal growth rate is assumed to be around zero. Anyone can assume any price cuts they want for any industry as an exercise, but how does biotech/biopharma end up with a terminal growth rate (future growth only five years, apparently) of about zero?

Well, Dr. Schoenebaum and DoctoRx appear to differ on that point. I'm more optimistic for the industry as being likely to experience secular growth.

Junior biotechs amplify the mood of the marginal investor. So if the terminal growth rate for the titans of the biotech industry is around zero, what hope is there for money-losing juniors?

The bearish/cautious views of Dr. Schoenebaum, Carl Icahn, and others are consistent with the implications of a behavioral indicator I have followed since it was introduced in the early part of this century, the Smith Barney "Other P/E" (Panic/Euphoria) indicator. When I a client of Smith Barney, I saw it work pretty well in real time. Now it's tough to get hold of, but this past Sunday I found a good technically-oriented blog that had a current version of it. It looks as though investors are deep in panic mode. In the past, this has been followed by a nicely higher stock market 12 months later. From The Fat Pitch:

While it's a little difficult to see (click to enlarge), the light blue line has just collapsed to deep panic levels. There are certainly no guarantees about the reliability of this indicator, but it fits the theme I'm seeing right now.

This chart was seen on Sunday, so it may or may not have included Friday's big down day, and it definitely did not include Monday's heavy selling pressure. So, it's possible that this indicator may show as much panic, or even a little more, than it measured at the bottom(s) in 2008-9.

The correlation of the SPY with these behavioral analyses may or may not continue to "work," and for sure they may have nothing to do with the action of any one specific sector.

Introduction - follow the cash burn and junk bond yields

One of the fundamental problems with junior biotechs is their need for new cash. Few new products on the market turn cash flow positive early on, so financing is needed for some time after a junior biotech succeeds in bringing a product to market. Any "risk off" episode with lower stock prices, rising sub-investment grade bond yields (i.e. declining prices of "junk" bonds) raises a company's financing costs, forces it to do some combination of additional shareholder dilution (including that of the insiders) and/or reduction of growth plans, and may negatively influence employee work effort.

In contrast, highly profitable majors such as Gilead can gain from these episodes. IPOs have already stopped. It may be easier to purchase a private company than a public one; and less expensive as well.

For this reason, the following charts of high-yield bonds has finally begun to correlate with the price action of the cash-burning junior biotechs. First, a large high-yield bond ETF (NYSEARCA:HYG):

This is pretty dismal. It's no surprise that directionally, XBI has finally begun moving in the same downward direction.

The credit spreads versus Treasury yields are also blowing out;

So, putting things together, it's no surprise that the double whammy of politically-induced (and sudden) worries about pricing and a major bear market in junk bonds has changed Mr. Market's method of valuing an unchanged set of unprofitable companies. Cost of and availability of capital have been worsening at the same time as a more cautious view of future pricing flexibility has begun to take hold.

Thinking through what a junior biotech stock represents

Yes, investing in a junior biotech is a form of gambling. However, I try to be like the young Bill Gross, who before building PIMCO up was a card-counter at Vegas and beat the house. So long as one is not investing in an extremely early-stage company (see my criticism of inappropriate IPOs above), here is what I look for in a company.

My bias is to think of this sort of investment as if it were an intermediate-term zero coupon bond, though with greater liquidity assuming the company is public. As with a zero, there is no possibility of current income. At some point, the company will either be generating sales/profits, or not. If not, the investment is a loser, though maybe not a complete wipe-out. If the company has succeeded in reaching a certain level, then unlike the zero coupon bond, where the upside is capped at par, the valuation of the stock has an infinite range. So it's my job as an investor to make projections based on known products that are planned to operate in established market niches (specific diseases, in most cases). And of course, the yields available on other sub-investment grade alternatives, such as junk bonds, must be considered. We all have our own hurdle rates for that sort of metric.

However, unlike Dr. Schoenebaum, I do not assume a terminal growth rate of zero for any biotech, large or small. I assume that the field will be viewed as a growth field 5-10 years from now.

Now, the "thing" about a zero coupon bond is that it either pays off or not. How it trades is not the point. The same is true of junior biotech stocks. Traders whip them around. As discussed above, sentiment swings manifest themselves most strongly not in the major biotechs , but in the juniors that have no discernible, measurable value as operating companies.

So, if sentiment gets very bearish, the greatest upside should come from the juniors if their stocks have been battered.

The other question that affects the juniors even more than the major biotechs is whether the government is really going to harm the industry. Are there really excess profits in biotech, or are there just a few sharpies dealing with old, non-biotech drugs, such as the recent Times article pointed to?

How likely is new Federal legislation that would be directly adverse to biotechs?

I believe that it's unlikely.

The pharmaceutical industry in general and biotech in specific provide a growing number of high-paying jobs that are located in the United States. Biotech companies contribute very positively to the country's balance of trade. This is a tough industry to deliberately hamper.

Recent history suggests biotech investors need not fear; any future legislative damage to the industry may already have either been incorporated or over-incorporated into stock prices.

To wit:

Even with a filibuster-proof majority in the Senate, the Democrats did not try to lay a glove on Big Pharma in the "Obamacare" legislation.

Before that, in 1994, some members of Big Pharma, including (if memory serves) Merck (NYSE:MRK) - the most influential pharma company at the time - were sympathetic to President Clinton's health care reform initiative. Then Hillary Clinton gave what I recall the New York Times referring to as the most bare-knuckled attack speech given by a First Lady in memory. That attack against the pharmaceutical industry angered Merck and may have doomed "Clintoncare."

It is not forgotten by today's politicians that the year of the Clintoncare failed legislation and the year Obamacare passed turned out to be mid-term election years that were historic disasters for the President's party.

So, from a brute political standpoint, there are easier industries to go after.

Also, politicians are people too. And when all is said and done, they want the best medicines for themselves and their families. They want breakthrough medicines as much as we all do.

As it happens, the Medicare Part D system does lead to price pressures on manufacturers, as providers set up their preferred drug networks. This battle was fought a decade ago, was not a point of controversy during the work-up of the Obamacare legislation, and would be difficult to alter via new legislation.

If constitutional, a narrow bit of legislation that addresses sudden, huge jumps in single-source drug prices might be achieved. That might not be an easy task, though.

Of course, anything can happen, but this recent stuff strikes me as typical political theater.

A word about XBI

I have often mentioned XBI, the SPDR S&P Biotech ETF, as a placeholder or example for junior biotechs. It's really not a pure junior biotech ETF. GILD is in it, and some non-biotech stocks are in it. But it will do as a proxy.

However, I am not bullish on XBI; that general feeling ended this summer, as has amply been described in several articles back then. Since feeling that the biotechs were primed for a summer fall, I have believed that specific company analysis going to prevail. So far, that has not worked, but we are still in the maelstrom. Specifically, they say that few battle plans survive contact with the enemy, and in this case, the pricing issue was not in my rational expectations playbook for the biotech sector. So be it. If politicians want to promise healthcare for the masses, they know that it's costly.

What many of them also know is that technology is deflationary when properly defined, and that applies to biotechnology as well. As an example and as a way of segueing to specific company discussion, let's take Opko (NYSE:OPK).

How Opko's product line exemplifies the difficulties facing would-be pharmaceutical cost controllers

OPK is the third major pharma vehicle for Dr. Phillip Frost, a 78-year old dermatologist. The first, Key Pharmaceuticals, was a pioneer in controlled-release drugs, and was sold in the mid-1980's to Schering-Plough.

OPK has been utterly crushed in the recent deluge, with Dr. Frost buying blocks of the stock on the way down. Note, while OPK is often considered a biotech, it's much more diversified than that. Its diversification, which includes a reference lab (via recent acquisition) and a diagnostic test for prostate cancer, makes it a good example of the difficulty politicians will have trying to bring down pharmaceutical prices.

First up, OPK acquired rolapitant, which had to be divested when MRK and Schering-Plough merged. The drug was not right for OPK to develop, and it found Tesaro (NASDAQ:TSRO), a young pharma company focusing on oncology, to take it through FDA approval. Rolapitant happily received FDA marketing approval as Varubi for prevention of chemo-induced nausea/vomiting a few weeks ago. It has generic competition in its class. In order for this drug to bring its benefits to patients, it has to have a long patent life and pricing flexibility. OPK had to have the incentive to buy the drug, and TSRO had to have the incentive to develop it with enough ROIC for OPK to receive royalty payments. Absent these conditions, it's quite possible that rolapitant never would have come to market. Eventually, of course, it will go generic and society will have permanent low-cost benefit from it. This sounds reasonable to me, not requiring new legislation.

Next up for OPK, Rayaldee. This is awaiting FDA approval. Rayaldee is said to be an improved formulation of (slightly simplifying for lay readers) vitamin D, with special benefits for many patients with kidney disease. Assuming this is an improved product that can successfully compete against the wide variety of vitamin D-like drugs already available, then Rayaldee will also return its profits into OPK and from OPK into the economy as a whole, then go generic and be available inexpensively to all who need it. Rejiggering the patent or pricing scheme to save a little money up front for payors could easily lead future products such as Rayaldee to simply not be developed.

Moving on to the last example, OPK is utilizing technology it acquired to develop a long-acting growth hormone. It has attracted Pfizer (NYSE:PFE) as its partner here. Instead of daily administration for today's growth hormone therapies, including PFE's own brand, the OPK version is given only once a week, also by subcutaneous injection. Presumably this will improve patient adherence and can cut drug acquisition cost by the payor, as well as greatly reducing the use of needles etc.

When I think of the chain of development of the controlled-release technology in this product, the ups and downs of the companies involved, and the commercial failure of at least one prior controlled-release growth hormone product despite FDA approval, I think that only an attractive patent and regulatory regime would attract further innovation in this product category. What would happen if the US made matters materially tougher for pharma companies would in my view be the off-shoring of a progressively greater percentage of product and pharma technology development - and soon.

So I just don't see it really happening, at least to any greater extent than the stocks have already priced in.

The above is not anything close to a full analysis of OPK, which has more going on than these drugs, including even more innovative products in earlier stages of development, as well as its large diagnostics business.

The point of discussing the three products discussed above is that they represent a spectrum of improved (or, allegedly improved) formulations or new chemical entities without which the world would keep spinning. Some or all of these products, which will become cheap at some point assuming they prove useful, may well never have come to public awareness. The absence of their development, at least their development by a US company in the US, would not be known. The lack of their development under different patent and pricing conditions fits with words from Bastiat:

In the economic sphere an act, a habit, an institution, a law produces not only one effect, but a series of effects. Of these effects, the first alone is immediate; it appears simultaneously with its cause; it is seen. The other effects emerge only subsequently; they are not seen; we are fortunate if we foresee them.

The benefits of price controls harsh enough to "move the needle" would be seen at once, and might even win an election. But I'm willing to invest on a scenario in which pharma and biotech innovation continues to be encouraged right here in the United States.

A more classic biotech junior is discussed next.

A (very) brief review of the biotech process: focus on Acceleron (NASDAQ:XLRN)

A Celgene affiliated-company, this company has been around many years. After years of effort, and extensive assistance from CELG (the top-rated pharma partnering company), one of its products is finally ready to enter Phase 3 testing for orphan diseases. This protein, luspatercept, is hoped to come to market for beta-thalassemia and myelodysplastic syndrome, two different anemias. A related drug, sotatercept, was recently disclosed by the CEO to be a "maybe" about advancement to Phase 3 for complications of renal failure with anemia. This "maybe" could be the cause of the stock sinking to an interim new closing low this week. XLRN is down from the high $50s, a price reached in the winter of 2014. Its action shows that the sector is not monolithic.

The stock has come down to earth. It could definitely go much lower, but I think it could also generate much larger profits over time than its market cap suggests, adjusted for an appropriate discount rate.

After all these years of research, XLRN is a $25 stock with an ex-cash market cap around $700 million. In several years, I think that its royalties from CELG could be well over $100 million per year and could grow from there, perhaps to hundreds of millions of dollars per year (it's really too early to get specific, though).

Luspatercept might fail in Phase 3 or surprise CELG and get approved but not succeed in the marketplace.

Given a growing pipeline, XLRN looks interesting to me.

At the least, if luspatercept comes to market, the current patent, regulatory and payment system will have brought a useful and even breakthrough medicine to benefit a group of people who through no fault of their own are suffering. Not only have many years of research, invention, blind alleys, etc. gone into the development of this one candidate, there still is nothing approaching certainty that anyone will ultimately make a dime off of it.

Whatever profits XLRN eventually generates, many years after embarking on its quest to make money the right way, by improving the world as we know it, will be justly earned. There will be no profiteering. I think Mr. Market knows this. (I bought more XLRN on this dip/crash, having sold most of my shares in the recent "rip" to $35.)

XLRN is a classic example of the risks and rewards of investing in a start-up wherein the only certainty is years of cash burn. This sort of investing is clearly not for all investors. It's my view, though, that it has led to robust improvements in pharmaceutical development that would not have occurred had the old way of Big Pharma driving almost all product development continued.

My expectation is that the US will continue to encourage this sort of risk-taking, for the greater good.

Summary and concluding thoughts - why pick on biotech?

In contrast to research-based pharmaceutical companies in general and biotechnology companies in specific, let's take a look at the tangible assets found in health insurers such as Aetna (NYSE:AET) and UnitedHealth (NYSE:UNH). But don't look too hard; summing up their tangible assets gives a negative number - less than XLRN.

What have these acquisitive giants actually contributed to human wellbeing to merit the future profits that are embodied in their stock market valuations? What have they invented? What risks have they taken?

Might America go the route of many other developed countries and remove all profits from the insurance business?

Wouldn't that actually save a lot of money?

The example of the refusal of the insurers to actually pay for hepatitis C cures in all patients with a prescription from a physician who wants to cure that patient suggests to me that these are not risk-based companies the way true insurers are. Rather, perhaps they are more like government-sponsored enterprises that make their money rationing care.

If Congress and the next President want to pick on a healthcare industry to save money, the health insurance industry is my candidate. Back in 2013, I correctly picked AET as a stock that could double - and it did. I'm out of it now, and for the robots that scan these articles to track the investment calls made by authors, I'm no longer bullish on AET.

We could be on the verge of a major wipe-out in the stock market. Those who "panicked" (i.e. sold) recently may have panicked correctly. Today could be like 1929, or worse. Or it could be 1998 or 2011, with months or years of upside price action and a growing economy ahead of us following a few months of downside price action.

As I see it, the junior biotech sector is one of the most dynamic of all parts of the US and global economy. It has been dumped on by political rhetoric, and the bears are growling loudly and publicly, both on the sector and the market. But their success comes from innovation, and only requires pricing within settled parameters to drive further investment. Absent that investment, progress in the sector will increasingly come from ex-US venues.

In addition, it's possible that the junk bond sector is seeing or has seen the worst of its troubles (that's not a prediction), especially the non-energy, non-mining/mineral high-yield bonds.

Thus both sentiment and one relevant fundamental might turn around, and perhaps soon.

After all, the world turns every 24 hours, and headlines change that fast as well. With that daily change can come, sooner or later, the realization that in the generally-mature US economy, it's pretty much only "tech" companies, plus "tech" as in biotech and related fields, that are true growth drivers right now. There's just not all that much innovation on a large scale elsewhere that I see as an investor who's always looking for new places to invest.

Thus I see the current bear market in junior biotechs as presenting interesting opportunities for new risk-oriented money that has a patient approach - though there may be great trading opportunities along the way. As stated, though, I have no special investing views on XBI or other small cap-oriented biotech funds; my analysis is of individual companies.

Note that risk is high, though, for all biotech stocks, and is magnified in the juniors. Trying to catch the falling knife can lead to a bloody outcome.

In a follow-up article planned to be completed and submitted to the editors soon, I'll present updates on a number of other junior biotechs.

Additional disclosure: Not investment advice. I am not an investment adviser.