Message Board")

Post by tomsylver on Aug 25, 2017 22:40:40 GMT

Two To Trade? MiMedX And Array

Aug. 25, 2017 2:57 PM ET|7 comments| About: Array BioPharma Inc. (ARRY), MDXG, Includes: GILD

(448 followers)

Summary

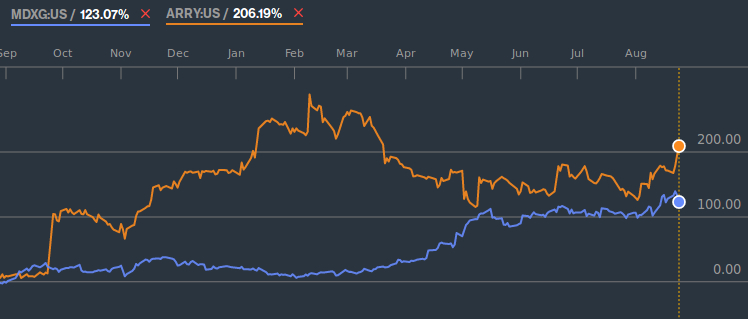

Their average share price is up an excellent 166%, whilst this figure over the year to date stands at 47.8%.

Array, with a market capitalization of $1.693bn, and currently trading at $9.50.

MiMedx is based in Georgia, has a market capitalization of $1.816bn, and presently trades at just under $17 per share.

As the weekend draws in, this article suggests two biotech stocks with a market capitalization of under $5bn that might be worth considering for your portfolio: MiMedx (MDXG), and Array BioPharma (ARRY). On average, over the past year, these companies have performed excellently. Their average share price is up an excellent 166%, whilst this figure over the year to date stands at 47.8%. Not bad for a year's work, and although biotech can be a volatile sector, the potential for long-term gains is significant. Gilead Science's (GILD) almost 5000% climb in 15 years is an example of how right things can go. With the biotech industry currently expected to climb in value to $727bn, growing at a CAGR of 7.4%, increasing your exposure to the sector might be a prudent choice.

MDXG, ARRY - Share Price 1 year. Source: Bloomberg

Array Biopharma:

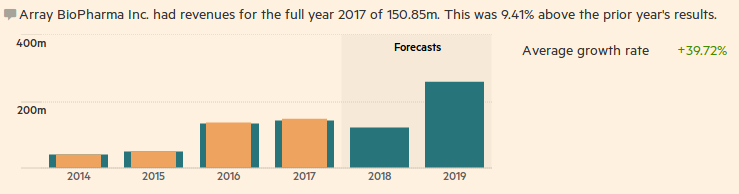

Yearly Revenue History & Forecasts - ARRY - Source: FT

Array, with a market capitalization of $1.693bn, and currently trading at $9.50, has recently had positive price targets reiterated by analysts at Piper Jaffray, Cantor Fitzgerald, and Stifel Nicolaus, with the average price target set at $13.30, a potential 40% upside. Array, based in Colorado, researches and develops targeted small molecule drugs to treat cancer, and has several promising products in the final stages of testing and development. Indeed, Array is expected to release data at the European Society for Medical Oncology soon, data which is expected to be positive. The future of the company looks bright, and although still loss making, revenues have risen for the past four years, and are up almost 10% this year. Cash reserves remain strong, up $69m, yet the company's debt-to-capital ratio is somewhat too high, at 91%.

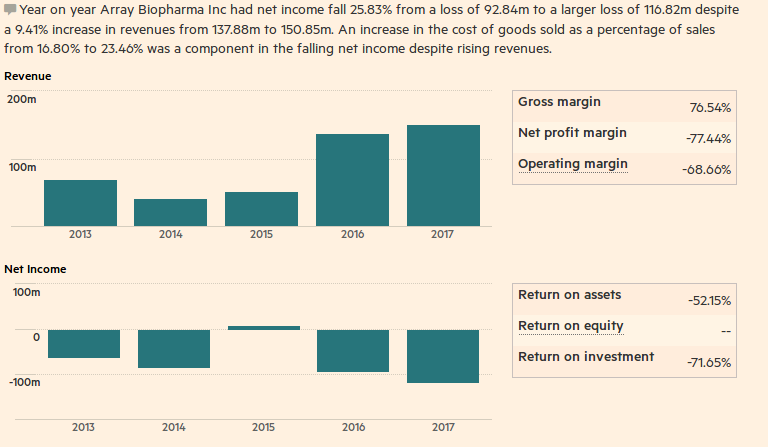

ARRY - Income Statement. Source: FT

The prime downside risk with regards to Array comes from, as might be expected, drug approval. Should its current melanoma drugs, binimetinib and encorafenib, fail to pass muster, the company's share price could take quite a hit. Yet, that said, with partners including Roche (OTCQX:RHHBY), Celgene (NASDAQ:CELG), Eli Lilly (NYSE:LLY), and AstraZeneca (NYSE:AZN), the biotech industry itself seems pretty sure of Array's future success. Furthermore, with Array's stock looking likely to break the psychological $10 barrier, a steady share price rise might well be on the cards. Indeed, with the market for MEK and BRAF inhibitors valued at $250m per quarter, should binimetinib and encorafenib gain FDA approval, Array is likely to see sustained growth.

ARRY - Analysts' Forecast. Source: FT

MiMedX:

MiMedX Revenue History & Estimates. Source: FT

MiMedx is an interesting company. There's something about bioactive healing, and tissue regeneration that sparks images of a future already here, yet having treated over 1,000,000 patients with its amniotic tissue grafts already, MiMedx already has plenty of experience. Essentially by recycling placental material, MiMedx deploys human amniotic membrane tissue to help to regenerate damaged or diseased tissues. The company is based in Georgia, has a market capitalization of $1.816bn, and presently trades at just under $17 per share. The company is growing, it is profitable, and it is performing, which certainly marks it out as a potential investment opportunity.

Earnings History & Estimates - MiMedx - Source: FT

Analysts, for instance, those at Piper Jaffray, suggest MiMedx has scope to grow, with a price target of $18, up 6% from its current level of just below $17 per share, whilst the company's financial data, especially for a biotech firm, is positive. The company's EPS, although not consistently climbing, has remained in the black for the past three years, and year-over-year comparisons with the last quarter show outstanding EPS growth of 250%. The company's current share price performance relative to the market (RSI) has been improving for several months, and its debt levels of 0.01% are excellent, meaning that MiMedx is a performing company, with essentially zero debt, in a growing industry. This surely marks it out as an interesting investment, as do its increasing cash reserves, which are up 20%. MiMedx certainly seems one to watch.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: CFDs, spread-betting and FX can result in losses exceeding your initial deposit. They are not suitable for everyone, so please ensure you understand the risks. Seek independent financial advice if necessary. Nothing in this article should be considered a personal recommendation. It does not account for your personal circumstances or appetite for risk.

Aug. 25, 2017 2:57 PM ET|7 comments| About: Array BioPharma Inc. (ARRY), MDXG, Includes: GILD

(448 followers)

Summary

Their average share price is up an excellent 166%, whilst this figure over the year to date stands at 47.8%.

Array, with a market capitalization of $1.693bn, and currently trading at $9.50.

MiMedx is based in Georgia, has a market capitalization of $1.816bn, and presently trades at just under $17 per share.

As the weekend draws in, this article suggests two biotech stocks with a market capitalization of under $5bn that might be worth considering for your portfolio: MiMedx (MDXG), and Array BioPharma (ARRY). On average, over the past year, these companies have performed excellently. Their average share price is up an excellent 166%, whilst this figure over the year to date stands at 47.8%. Not bad for a year's work, and although biotech can be a volatile sector, the potential for long-term gains is significant. Gilead Science's (GILD) almost 5000% climb in 15 years is an example of how right things can go. With the biotech industry currently expected to climb in value to $727bn, growing at a CAGR of 7.4%, increasing your exposure to the sector might be a prudent choice.

MDXG, ARRY - Share Price 1 year. Source: Bloomberg

Array Biopharma:

Yearly Revenue History & Forecasts - ARRY - Source: FT

Array, with a market capitalization of $1.693bn, and currently trading at $9.50, has recently had positive price targets reiterated by analysts at Piper Jaffray, Cantor Fitzgerald, and Stifel Nicolaus, with the average price target set at $13.30, a potential 40% upside. Array, based in Colorado, researches and develops targeted small molecule drugs to treat cancer, and has several promising products in the final stages of testing and development. Indeed, Array is expected to release data at the European Society for Medical Oncology soon, data which is expected to be positive. The future of the company looks bright, and although still loss making, revenues have risen for the past four years, and are up almost 10% this year. Cash reserves remain strong, up $69m, yet the company's debt-to-capital ratio is somewhat too high, at 91%.

ARRY - Income Statement. Source: FT

The prime downside risk with regards to Array comes from, as might be expected, drug approval. Should its current melanoma drugs, binimetinib and encorafenib, fail to pass muster, the company's share price could take quite a hit. Yet, that said, with partners including Roche (OTCQX:RHHBY), Celgene (NASDAQ:CELG), Eli Lilly (NYSE:LLY), and AstraZeneca (NYSE:AZN), the biotech industry itself seems pretty sure of Array's future success. Furthermore, with Array's stock looking likely to break the psychological $10 barrier, a steady share price rise might well be on the cards. Indeed, with the market for MEK and BRAF inhibitors valued at $250m per quarter, should binimetinib and encorafenib gain FDA approval, Array is likely to see sustained growth.

ARRY - Analysts' Forecast. Source: FT

MiMedX:

MiMedX Revenue History & Estimates. Source: FT

MiMedx is an interesting company. There's something about bioactive healing, and tissue regeneration that sparks images of a future already here, yet having treated over 1,000,000 patients with its amniotic tissue grafts already, MiMedx already has plenty of experience. Essentially by recycling placental material, MiMedx deploys human amniotic membrane tissue to help to regenerate damaged or diseased tissues. The company is based in Georgia, has a market capitalization of $1.816bn, and presently trades at just under $17 per share. The company is growing, it is profitable, and it is performing, which certainly marks it out as a potential investment opportunity.

Earnings History & Estimates - MiMedx - Source: FT

Analysts, for instance, those at Piper Jaffray, suggest MiMedx has scope to grow, with a price target of $18, up 6% from its current level of just below $17 per share, whilst the company's financial data, especially for a biotech firm, is positive. The company's EPS, although not consistently climbing, has remained in the black for the past three years, and year-over-year comparisons with the last quarter show outstanding EPS growth of 250%. The company's current share price performance relative to the market (RSI) has been improving for several months, and its debt levels of 0.01% are excellent, meaning that MiMedx is a performing company, with essentially zero debt, in a growing industry. This surely marks it out as an interesting investment, as do its increasing cash reserves, which are up 20%. MiMedx certainly seems one to watch.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: CFDs, spread-betting and FX can result in losses exceeding your initial deposit. They are not suitable for everyone, so please ensure you understand the risks. Seek independent financial advice if necessary. Nothing in this article should be considered a personal recommendation. It does not account for your personal circumstances or appetite for risk.