Message Board")

Post by tomsylver on Nov 21, 2018 15:15:34 GMT

Tesaro Is Now An Attractive Acquisition Target

Nov. 21, 2018 5:18 AM ET|

Tim Erickson

Long/short equity, biotech, Cancer Immunotherapy

Summary

* Tesaro is well-positioned to steal a significant portion of the massive lung cancer market from Bristol-Myers Squibb and Merck.

* PD-1/TIM-3 chemo combo could become the SoC in 1L NSCLC in 3 years.

* Gilead and Roche are the most likely suitors, as they could greatly benefit from a best-in-class PD-1 antibody like TSR-042.

Several months ago, I wrote an SA article on Tesaro (NASDAQ:TSRO) warning investors of an imminent decline in the stock due to lingering concerns regarding Zejula's safety, competition and its massive cash burn issue. At the time, TSRO was trading near $60/share and subsequently lost more than half its value, reaching a 52-week low of $23.41 prior to the recent rumor-driven rebound.

TSR-042/TSR-022 Have Strong Potential for 1L NSCLC

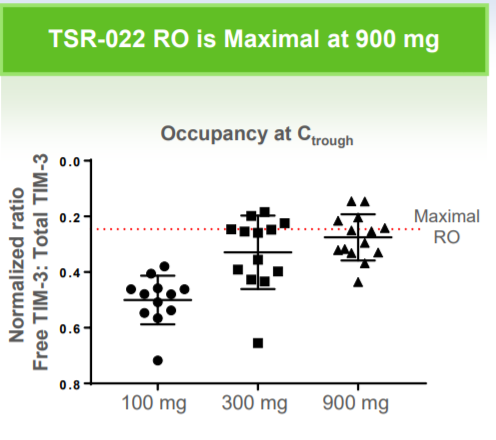

TSRO recently presented data from its anti-PD-1 (TSR-042)+anti-TIM-3 (TSR-022) AMBER trial in NSCLC at SITC. Notably, the trial enrolled patients who had progressed on prior anti-PD-1 antibodies, including Bristol-Myers Squibb's (NYSE:BMY) Opdivo (nivolumab) and Merck's (NYSE:MRK) Keytruda (pembrolizumab). The majority of patients had already exhausted third- and fourth-line therapies. In AMBER, data is available for both the 100 mg and 300 mg doses of TSR-022 in combination with TSR-042. The 100 mg dose showed relatively poor efficacy, likely due to insufficient receptor occupancy (50% at the pharmacokinetic trough). In other words, the 100 mg dose did not provide enough antibody to block TIM-3's interaction with its putative ligand. However, at the higher dose (300 mg), receptor occupancy was much higher (~75%) and activity was notable. In the PD-1 TPS>1% subset (~60% of patients), TSRO-022 provided a 33% response rate and a clinical benefit rate exceeding 50%.

Huge Upside In NSCLC

Notably, the enhanced efficacy and lack of safety concerns strongly imply that TSRO could run a head-to-head trial comparing TSR-042+TSR-022+chemo vs. Keytruda+chemo and become the standard of care (SoC) in 1L NSCLC. The trial would likely take 3 years to run, but would likely be a very lucrative win for Tesaro. Given 150,000 cases/year in the US and assuming a conservative 20% market share, this would amount to 30,000 patients treated. Drug prices for monoclonal antibodies are a bit insane, in my opinion ($152,000 per year for Keytruda), so applying the same price to TSR-022+TSR-042 in value-driven pricing would yield revenues of at least $4.5 billion. Adding in $300 million from Zejula and $300 million for TSR-042 in endometrial and MSI-high tumors gives the company total revenues of $5.1 billion. Assuming a 3x-4x sales multiple typical of biopharma companies, this gives a potential future value of $15-20 billion. Not a bad deal for paying 3-4 billion upfront. Furthermore, this simple calculation excludes additional revenues due to longer response times of ovarian cancer patients treated with Zejula in earlier lines of therapy in combination with TSR-042 and/or Avastin.

While it is true that TSRO will face competition from other agents in NSCLC, including Opdivo+peg-IL2 by Nektar Therapeutics (NASDAQ:NKTR) or Keytruda+peg-IL10, it is likely that TIM-3 blockade could be further combined with these agents down the road to further improve the SoC. TSRO is the first to report clinical trial data on combined PD-1/TIM-3 blockade, and therefore, has first-mover advantage. Additionally, the company has engineered a patient-centric dosing scheme. After the first 4 doses, patients only require antibody infusions every 6 weeks for TSR-042, versus 3 weeks for Keytruda and 2 weeks for Opdivo. Extra competition and fewer clinical visits is the kind of innovation our health system needs to drive down prices without government price-fixing. If Tesaro undercuts Merck's pricing on Keytruda, Medicare might consider writing the company a Thank You note. So yes, Tesaro's IO assets are a legitimate threat to Merck's crown jewel in NSCLC.

As icing on the cake, PD-1/TIM-3 are checkpoints known to hinder the efficacy of CAR-T therapy. While CAR-T cells could theoretically be engineered with silenced PD-1/TIM-3 genes, this is easier said than done (nothing currently in clinical trials). Thus, there is a strong rationale that these agents would be needed to increase the response rate and duration of response of CAR-T therapy in solid tumors by reversing or limiting T-cell exhaustion.

Numerous large drug companies have growing ambitions in cancer immunotherapy, including Gilead (NASDAQ:GILD) and Roche (OTCQX:RHHBY). GILD currently lacks an approved PD-1 antibody and will likely need one to maximize revenue from its CAR-T ambitions in solid tumors. While Roche has anti-PDL1 atezolizumab, its efficacy has generally lagged PD-1 antibodies. Given its current collaboration with TSRO's Zejula in bladder cancer, it might make sense for Roche to buy Tesaro at a discount and bolster its lagging lung cancer fortunes with best-in-class assets. Both Roche and Gilead have the cash flows to fund pivotal Phase III clinical trials and the clinical leverage to speed up trial recruitment.

It will be interesting to see how things play out in the coming days, but from a valuation perspective, it makes sense for Tesaro to get acquired. Despite having compelling assets, company management has done a horrible job of managing cash burn. SG&A has exceeded Zejula revenue in every quarter, so Tesaro sits at a crossroads. Absent a bidding war which leads to a buyout, Tesaro will continue to burn cash and likely be forced to substantially dilute shareholders, unless management finds ways to cut $200 million a year from its bloated budget.

The company deserves applause for developing compelling assets which hold great future value. If the company had managed cash more conservatively since IPO, it could be sitting on a comfortable cushion, ready to pounce on large markets. Shareholders have suffered due to some mismanagement, particularly in regard to Varubi and initially selecting a toxic dose of Zejula (300 mg versus 200 mg currently used in most studies), but the IO pipeline development is going extremely well.

In the face of tough IO competition, Tesaro has used its R&D budget to advance assets at a rapid pace. I believe that shareholders will soon be rewarded with a buyout or continued appreciation of TSRO shares as the market prices in the increased likelihood of multi-billion dollar future revenues for a company currently trading at ~$2 billion, a fraction of Merck's Keytruda revenue in lung cancer. While there are numerous PD-1 antibodies in development, including those from Incyte Corp. (NASDAQ:INCY), Agenus (NASDAQ:AGEN) and others, the documented activity of TSR-042+TSR-022 in Keytruda/Opdivo refractory patients is a major factor motivating a buyout. TSRO may have a second-rate PARP inhibitor, but best-in-class PD-1/TIM-3 antibodies. The market for the latter is much larger than for the former.

Disclosure: I am/we are long TSRO.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Nov. 21, 2018 5:18 AM ET|

Tim Erickson

Long/short equity, biotech, Cancer Immunotherapy

Summary

* Tesaro is well-positioned to steal a significant portion of the massive lung cancer market from Bristol-Myers Squibb and Merck.

* PD-1/TIM-3 chemo combo could become the SoC in 1L NSCLC in 3 years.

* Gilead and Roche are the most likely suitors, as they could greatly benefit from a best-in-class PD-1 antibody like TSR-042.

Several months ago, I wrote an SA article on Tesaro (NASDAQ:TSRO) warning investors of an imminent decline in the stock due to lingering concerns regarding Zejula's safety, competition and its massive cash burn issue. At the time, TSRO was trading near $60/share and subsequently lost more than half its value, reaching a 52-week low of $23.41 prior to the recent rumor-driven rebound.

Prior takeover talk happened when TSRO traded at a rich valuation level of ~$10 billion. At the current ~$2 billion valuation, I believe it trades at a compelling valuation and will eventually be bought out north of $50/share. Here is my reasoning.

TSRO recently presented data from its anti-PD-1 (TSR-042)+anti-TIM-3 (TSR-022) AMBER trial in NSCLC at SITC. Notably, the trial enrolled patients who had progressed on prior anti-PD-1 antibodies, including Bristol-Myers Squibb's (NYSE:BMY) Opdivo (nivolumab) and Merck's (NYSE:MRK) Keytruda (pembrolizumab). The majority of patients had already exhausted third- and fourth-line therapies. In AMBER, data is available for both the 100 mg and 300 mg doses of TSR-022 in combination with TSR-042. The 100 mg dose showed relatively poor efficacy, likely due to insufficient receptor occupancy (50% at the pharmacokinetic trough). In other words, the 100 mg dose did not provide enough antibody to block TIM-3's interaction with its putative ligand. However, at the higher dose (300 mg), receptor occupancy was much higher (~75%) and activity was notable. In the PD-1 TPS>1% subset (~60% of patients), TSRO-022 provided a 33% response rate and a clinical benefit rate exceeding 50%.

(Source: Company Presentation 11/12/18)

Now, it is critical to reiterate that these were very sick patients who had already progressed on Opdivo or Keytruda. They were out of options and for about 50%, TIM-3 appeared to provide significant benefit. And importantly, there were no major safety signals in the combo. Even better, TSRO is currently testing a 900 mg dose of TSR-022, which should provide maximal receptor occupancy and improved efficacy. The activity of TSR-022 jives well with preclinical data showing that combined PD-1/TIM-3 blockade can rescue exhausted T-cells in NSCLC tumors and improve OS.

Notably, the enhanced efficacy and lack of safety concerns strongly imply that TSRO could run a head-to-head trial comparing TSR-042+TSR-022+chemo vs. Keytruda+chemo and become the standard of care (SoC) in 1L NSCLC. The trial would likely take 3 years to run, but would likely be a very lucrative win for Tesaro. Given 150,000 cases/year in the US and assuming a conservative 20% market share, this would amount to 30,000 patients treated. Drug prices for monoclonal antibodies are a bit insane, in my opinion ($152,000 per year for Keytruda), so applying the same price to TSR-022+TSR-042 in value-driven pricing would yield revenues of at least $4.5 billion. Adding in $300 million from Zejula and $300 million for TSR-042 in endometrial and MSI-high tumors gives the company total revenues of $5.1 billion. Assuming a 3x-4x sales multiple typical of biopharma companies, this gives a potential future value of $15-20 billion. Not a bad deal for paying 3-4 billion upfront. Furthermore, this simple calculation excludes additional revenues due to longer response times of ovarian cancer patients treated with Zejula in earlier lines of therapy in combination with TSR-042 and/or Avastin.

While it is true that TSRO will face competition from other agents in NSCLC, including Opdivo+peg-IL2 by Nektar Therapeutics (NASDAQ:NKTR) or Keytruda+peg-IL10, it is likely that TIM-3 blockade could be further combined with these agents down the road to further improve the SoC. TSRO is the first to report clinical trial data on combined PD-1/TIM-3 blockade, and therefore, has first-mover advantage. Additionally, the company has engineered a patient-centric dosing scheme. After the first 4 doses, patients only require antibody infusions every 6 weeks for TSR-042, versus 3 weeks for Keytruda and 2 weeks for Opdivo. Extra competition and fewer clinical visits is the kind of innovation our health system needs to drive down prices without government price-fixing. If Tesaro undercuts Merck's pricing on Keytruda, Medicare might consider writing the company a Thank You note. So yes, Tesaro's IO assets are a legitimate threat to Merck's crown jewel in NSCLC.

As icing on the cake, PD-1/TIM-3 are checkpoints known to hinder the efficacy of CAR-T therapy. While CAR-T cells could theoretically be engineered with silenced PD-1/TIM-3 genes, this is easier said than done (nothing currently in clinical trials). Thus, there is a strong rationale that these agents would be needed to increase the response rate and duration of response of CAR-T therapy in solid tumors by reversing or limiting T-cell exhaustion.

Numerous large drug companies have growing ambitions in cancer immunotherapy, including Gilead (NASDAQ:GILD) and Roche (OTCQX:RHHBY). GILD currently lacks an approved PD-1 antibody and will likely need one to maximize revenue from its CAR-T ambitions in solid tumors. While Roche has anti-PDL1 atezolizumab, its efficacy has generally lagged PD-1 antibodies. Given its current collaboration with TSRO's Zejula in bladder cancer, it might make sense for Roche to buy Tesaro at a discount and bolster its lagging lung cancer fortunes with best-in-class assets. Both Roche and Gilead have the cash flows to fund pivotal Phase III clinical trials and the clinical leverage to speed up trial recruitment.

It will be interesting to see how things play out in the coming days, but from a valuation perspective, it makes sense for Tesaro to get acquired. Despite having compelling assets, company management has done a horrible job of managing cash burn. SG&A has exceeded Zejula revenue in every quarter, so Tesaro sits at a crossroads. Absent a bidding war which leads to a buyout, Tesaro will continue to burn cash and likely be forced to substantially dilute shareholders, unless management finds ways to cut $200 million a year from its bloated budget.

The company deserves applause for developing compelling assets which hold great future value. If the company had managed cash more conservatively since IPO, it could be sitting on a comfortable cushion, ready to pounce on large markets. Shareholders have suffered due to some mismanagement, particularly in regard to Varubi and initially selecting a toxic dose of Zejula (300 mg versus 200 mg currently used in most studies), but the IO pipeline development is going extremely well.

In the face of tough IO competition, Tesaro has used its R&D budget to advance assets at a rapid pace. I believe that shareholders will soon be rewarded with a buyout or continued appreciation of TSRO shares as the market prices in the increased likelihood of multi-billion dollar future revenues for a company currently trading at ~$2 billion, a fraction of Merck's Keytruda revenue in lung cancer. While there are numerous PD-1 antibodies in development, including those from Incyte Corp. (NASDAQ:INCY), Agenus (NASDAQ:AGEN) and others, the documented activity of TSR-042+TSR-022 in Keytruda/Opdivo refractory patients is a major factor motivating a buyout. TSRO may have a second-rate PARP inhibitor, but best-in-class PD-1/TIM-3 antibodies. The market for the latter is much larger than for the former.

Disclosure: I am/we are long TSRO.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.