Message Board")

TSRO SA: In The Middle Of A Difficulty Is An Opportunity

Nov 13, 2018 15:46:08 GMT

icemandios likes this

Post by tomsylver on Nov 13, 2018 15:46:08 GMT

Tesaro: In The Middle Of A Difficulty Is An Opportunity

Nov. 13, 2018 9:38 AM ET |

* An excellent place to search for bargain stocks is to assess equities that experienced a big decline subsequent to a market-moving event.

* While a huge depreciation can signal organic problems, there are situations in which the market simply misinterpreted a corporate event and thus discounted an excellent firm.

* Tesaro recently suffered an over 18% loss in its market valuation amidst what are strong fundamental developments.

* Investors should look at the 2018 Society for Immunotherapy of Cancer data that Tesaro presented in its appropriate context.

* The most value resides in Zejula. And, its potential approval as the 1st-line treatment for ovarian and prostate cancers can ramp up revenues by leaps and bound.

"There is no better teacher than history in determining the future... There are answers worth billions of dollars in $30 history book." - Charlie Munger

In leveraging on the “opportunistic” element of Integrated BioSci Investing, we love to check out bioscience stocks that suffered a significant decline. While there are legitimate reasons that cause a stock to tumble, certain situations exist in which the market simply overreacts: this creates an excellent entry point for investors wishing to build shares in a good business. That’s what we believe happened to Tesaro (NASDAQ:TSRO), an oncology-focused operator that recently presented its clinical data at the 2018 Society for Immunotherapy of Cancer (“SITC”) Annual Meeting. It is most likely that the market interpreted the response rates of (TSR-022 and -042) without their appropriate context. Moreover, it can be quite early to stake conclusive claims about the clinical outcomes of those early-stage molecules. Amid the said difficulty, the rapid advancement of Tesaro’s flagship product (Zejula) should continue to unlock substantial values for patients and shareholders alike. In this research, we’ll take a deep-dive analysis on the latest data release, the Zejula franchise, and upgrade our bull thesis on this growth company.

Figure 1: Tesaro chart (Source: StockCharts)

As usual, we’ll provide a brief overview of the company for new investors. If you are already familiar with the firm, we recommend that you skip to the subsequent section. We noted in the prior research:

"Based in Waltham MA, Tesaro is focused on the innovation and commercialization of novel molecules to manage various cancers as shown in Figure 2. The lead drug (Zejula) is approved and commercialized in both the U.S. and EU. Since launched in April 2017, Zejula is the most prescribed PARP inhibitor (as a maintenance therapy for patients afflicted by ovarian cancer in the U.S., who demonstrated the complete or partial responses to platinum-based chemotherapy). Moreover, the EU launch of niraparib (Zejula) continues in Germany. Zejula sales are improving drastically to provide a meaningful revenues stream to power other pipeline innovation. Asides from Zejula, there is another commercialized molecule, rolapitant (Varubi) that is approved as a prevention of the delayed chemotherapy-induced nausea and vomiting."

2018 SITC Data Presentation

AMBER

As an ongoing Phase 1 study, AMBER investigates the efficacy and safety of TSR-022 (an anti-TIM3) and TSR-042 (an anti-PD-1) monoclonal antibodies in two groups (i.e. cohorts) of patients. Of note, these patients had prior anti-PD-1 treatment yet their tumors are still progressing. As follows, one group has the deadly non-small cell lung cancer (“NSCLC”) while the other cohort has advanced melanoma (a potentially lethal skin cancer).

Per trial design, the patients are dosed with TSR-042 500mg in combinations with either TSR-022 100mg or 300mg every 3 weeks. At the data cutoff, one in 14 patients with NSCLC responded at the TSR-022 100mg dose (i.e., a 9% partial response rate). Interestingly, the partial response rate improved to 15% (3/20 patients) at the higher dose (i.e., TSR-022 400mg). Therefore, the data indicates that there is a “dose-response” relationship which underlies therapeutic efficacy. In our view, it’s very likely that there will be a 33% response rate at the 900mg dose because we noticed that the addition of 200mg increment raised the response rate by 6%

GARNET

In contrast to AMBER, the ongoing Phase 1 GARNET study assesses TSR-042 alone in patients suffering from advanced solid tumors, including endometrial cancer, and recurrent NSCLC. Notably, patients are dosed with TSR-042 500mg every 3 weeks. The data at SITC only entails patients with NSCLC because their dosing is completed. Of 47 patients, 15 people experienced partial responses and thereby represents a 32% rate. There was also a 29.8% stable disease rate (14/47 patients). More interestingly, the responses were durable for 9/15 patients (i.e., a 60% ongoing response rate)

CITRINO

Assessment Of The Third-Quarter Earnings

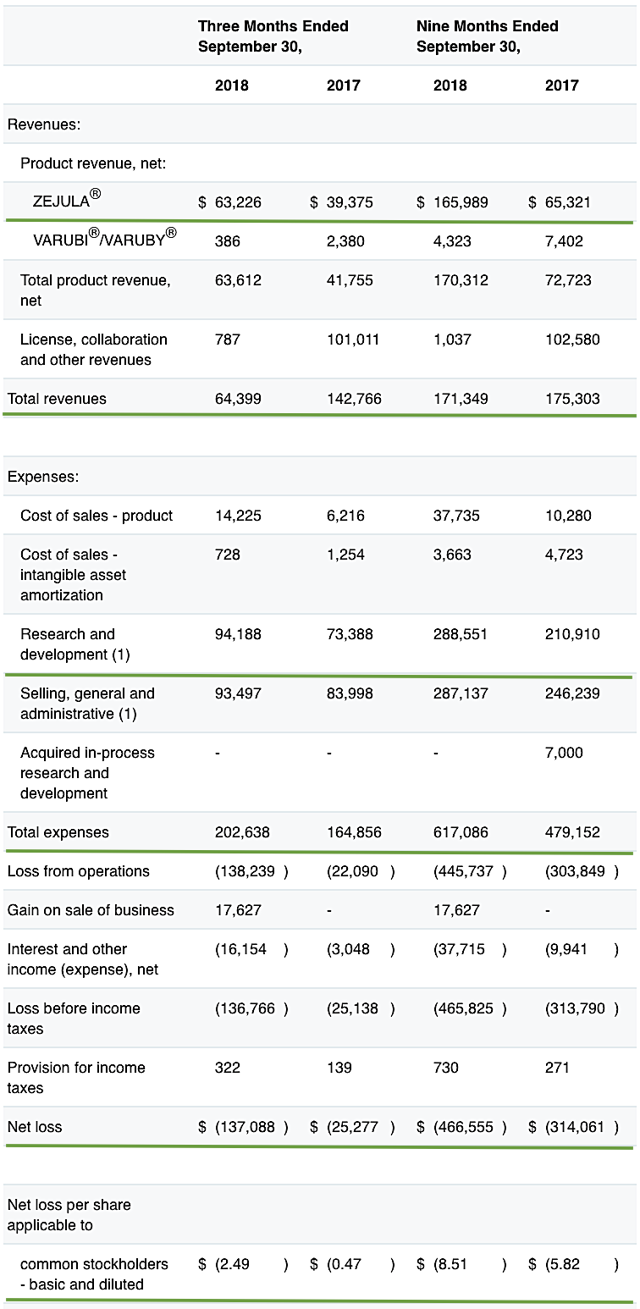

As earnings revealed many developments, we’ll assess the latest earnings report. For the third-quarter earnings that ended on Sept. 30, 2018, Tesaro posted $63.6M in revenues compared to $41.8M for the same period a year prior. This signifies a 52.1% year-over-year improvement. Nearly all revenues came from Zejula.

Figure 3: Key financial metrics (Source: Tesaro, adapted by Integrated BioSci Investing)

Additionally, there were $137.1M ($2.49 per share) net losses versus $25.3M ($0.47 per share) declines. This signifies a 429% worsening in the bottom line earnings. Nevertheless, investors should be cognizant that it is the norm for a relatively young bioscience company like Tesaro to incur significant losses for years prior to banking a net profit (due to the lengthy and low success rate of the innovation process). That aside, the research and development (R&D) for the respective periods came in at $94.2M and $73.4M, thus representing a 28% increase. We generally view an increase in R&D positively because the R&D money committed today - while reducing the net earnings - can turn into significant profits tomorrow.

Catalyst Tracking

Earnings aside, it is important for investors to keep tab on the ongoing corporate developments for you to know what to expect from your business. Therefore, we track the pertinent catalysts in Table 1 below. The most important event is the top-line reporting for PRIMA that is anticipated in late 2019. PRIMA is a Phase 3 study of Zejula for pushing the said drug into the 1st-line indication for ovarian cancer. We strongly believe that this crucial catalyst will enable Tesaro to ramp up niraparib revenues by multiple folds. This is because most of the blockbuster drugs are 1st-line medicine. Commenting on the recent developments, the CEO (Lonnie Moulder) enthused:

"In the third quarter, we launched several initiatives to grow the use of Zejula for recurrent ovarian cancer and we continued to execute on our development strategies focused on gynecologic and lung cancers as we approach a period of significant data readouts. Following results of the Phase 3 PRIMA trial next year, we intend for Zejula to benefit patients throughout all stages of their ovarian cancer journey, including First-line, recurrent, and late-line treatment settings. Our immuno-oncology pipeline continues to advance, led by our anti-PD-1 antibody, TSR-042, for which we are on track to submit a BLA next year. We look forward to initial data from the Phase 1 AMBER trial of our anti-TIM-3 antibody, TSR-022, in combination with TSR-042, which will be presented at SITC Annual Meeting next week."

Latest developments

Clinical

Results of GARNET were presented at ESMO with TSR-042 well-tolerated and demonstrated the encouraging efficacy for endometrial cancer.

The $18M milestone payment earned for the advancement of GALAHAD (a trial that studies niraparib in metastatic castration-resistant prostate cancer). This is also quite important to the future revenues increase for Zejula.

Other

Zejula revenues improved by 61% year over year. Zejula is now approved in 33 countries worldwide.

Zai Lab announced the Zejula approval in Hong Kong on Oct. 22, 2018.

Tesaro and actress Cobie Smulders launched, “Not on My Watch” to empowered the ovarian cancer community.

Outlook

The top-line results for PRIMA trial studying Zejula monotherapy as the 1st-line treatment for ovarian cancer are expected in late 2019.

TSR-042 BLA submission is projected for H2 2019.

Quantitative Data Forecasting

As the PRIMA endpoints are crucial to the future revenues increase, we’ll conduct a clinical forecasting for the aforesaid Phase 3 trial. Leveraging our Integrated BioSci framework of “molecule analysis” - that took into accounts different scoring variables, including available trial data (“TDV”), comparative molecular analysis (“CMV”), structural design (“SDV”), clinical trial setups (“TSV”), and disease specificity ("DSV") - we prognosticated that there are over 65% chances that Zejula will procure positive outcomes, thereby indicating a “more than favorable” reporting.

Notably, TDV and DSV factored substantially into this data forecast. The prior Zejula data is stellar to enable its approval as a maintenance therapy for ovarian cancer in 33 countries: it is the major determinant to PRIMA success. In other words, it is reasonable to expect the aforesaid drug to achieve similar findings in this trial.

Regarding qualitative analysis as shown in Table 2, Zejula scored a high rating on scientific novelty because a PPAR inhibitor is novel yet it is not as exotic as CAR-T or gene therapy. Nevertheless, we rated the unmet medical needs extremely high, because the death rate for advanced/resistant ovarian cancer is “off the roof.” This is one of the deadliest cancer. Taken altogether, there should be an extremely high ease of regulatory approval. Moreover, the stellar FDA Commissioner (Dr. Scott Gottlieb) lowered the regulatory hurdles to enable an unprecedented delivery of life-saving therapeutics to patients which should help out Zejula.

Qualitative analysis for Zejula

Scientific novelty (product differentiation) High

Unmet medical needs (therapeutic demand) Extremely high

Ease of regulatory approval Extremely high

Valuations

Warren Buffett stated that two excellent analysts can assess the same company and come up with distinct figures. Hence, one should take valuation within its appropriate context. To minimize subjectivity, we employed the comparative market analytical method (of gauging similar firms to give investors a rough estimate of an investment’s value). We usually check the Wall Street analysts consensus estimate to get the market sentiment on a particular stock. That said, Wall Street put the $56 price target (“PT”) on Tesaro.

In the next step, we’ll appraise Tesaro based on our estimated potential sales for Zejula (as the 1st line treatment for both ovarian and prostate cancers). And, we’ll take into account the 10 price to earnings (P/E) ratio, 54.9M shares outstanding, a 25% profit margin, and a 35% discount. Of note, we discounted this franchise by 35% due its chances of clinical and regulatory failure. The stellar Zejula quality and the large combined (prostate and ovarian cancers) market should yield the estimated potential revenues ranging from $1B to $2.5B.

Zejula in first

line ovarian $1B $250M $45.53 $29.59

Zejula in first

Table 3: Valuation analysis (Source: Integrated BioSci Investing)

Potential Risks

Conclusion

In all, we raised our recommendation on Tesaro from a speculative buy to a buy. We also increased our rating from three to four stars. And, we augmented our (two to three years) PT from $50 to $51.79 to be most representative of our valuation. Tesaro is powered by a superb approved-drug, Zejula that is scientifically and clinically validated. It is already being used as a maintenance therapy for ovarian cancers yet the company is increasing its launch efforts. Even better is that Tesaro is pushing Zejula into a 1st-line drug for ovarian cancer that, in and of itself, will unlock the most value for the company. That aside, Zejula is being advanced as a drug for metastatic prostate cancer which has a huge market. Our research on another company, Clovis Oncology (NASDAQ:CLVS) demonstrated that PPAR inhibition can be an excellent approach to treating prostate cancer. Regarding the latest data for other pipeline medicines (TSR-022, -042, and -033), the early data are promising in our views. Nonetheless, the market usually expects “home run” results. Therefore, the recent share price depreciation indeed created an excellent entry point for investors wishing to get in this highly promising company.

About Integrated BioSci Investing

We’re honored that you visited us. Founded by Dr. Hung Tran, MD, MS, CNPR, IBI is uncovering big winners. For instance, Nektar, Spectrum, Madrigal, Atara, and Kite procured +94%, +69%, +127%, +138%, and +83%, respectively. Our secret sauce is extreme due diligence with expert data analysis. The service features daily research/consulting. While we publish some ideas publicly, those articles are available in advance and are discussed more extensively in IBI. We also reserve our best ideas exclusively for IBI members. And, we invite you to subscribe now to lock in the current price.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: As a medical doctor/market expert, Dr. Tran is not a registered investment advisor. Despite that we strive to provide the most accurate information, we neither guarantee the accuracy nor timeliness. Past performance does NOT guarantee future results. We reserve the right to make any investment decision for ourselves and our affiliates pertaining to any security without notification except where it is required by law. We are also NOT responsible for the action of our affiliates. The thesis that we presented may change anytime due to the changing nature of information itself. Investing in stocks and options can result in a loss of capital. The information presented should NOT be construed as recommendations to buy or sell any form of security. Our articles are best utilized as educational and informational materials to assist investors in your own due diligence process. That said, you are expected to perform your own due diligence and take responsibility for your action. You should also consult with your own financial advisor for specific guidance, as financial circumstances are individualized.

Nov. 13, 2018 9:38 AM ET |

BioSci Capital Partners

Summary

* An excellent place to search for bargain stocks is to assess equities that experienced a big decline subsequent to a market-moving event.

* While a huge depreciation can signal organic problems, there are situations in which the market simply misinterpreted a corporate event and thus discounted an excellent firm.

* Tesaro recently suffered an over 18% loss in its market valuation amidst what are strong fundamental developments.

* Investors should look at the 2018 Society for Immunotherapy of Cancer data that Tesaro presented in its appropriate context.

* The most value resides in Zejula. And, its potential approval as the 1st-line treatment for ovarian and prostate cancers can ramp up revenues by leaps and bound.

Looking for more? I update all of my investing ideas and strategies to members of Integrated BioSci Investing. Start your free trial today »

"There is no better teacher than history in determining the future... There are answers worth billions of dollars in $30 history book." - Charlie Munger

In leveraging on the “opportunistic” element of Integrated BioSci Investing, we love to check out bioscience stocks that suffered a significant decline. While there are legitimate reasons that cause a stock to tumble, certain situations exist in which the market simply overreacts: this creates an excellent entry point for investors wishing to build shares in a good business. That’s what we believe happened to Tesaro (NASDAQ:TSRO), an oncology-focused operator that recently presented its clinical data at the 2018 Society for Immunotherapy of Cancer (“SITC”) Annual Meeting. It is most likely that the market interpreted the response rates of (TSR-022 and -042) without their appropriate context. Moreover, it can be quite early to stake conclusive claims about the clinical outcomes of those early-stage molecules. Amid the said difficulty, the rapid advancement of Tesaro’s flagship product (Zejula) should continue to unlock substantial values for patients and shareholders alike. In this research, we’ll take a deep-dive analysis on the latest data release, the Zejula franchise, and upgrade our bull thesis on this growth company.

As usual, we’ll provide a brief overview of the company for new investors. If you are already familiar with the firm, we recommend that you skip to the subsequent section. We noted in the prior research:

"Based in Waltham MA, Tesaro is focused on the innovation and commercialization of novel molecules to manage various cancers as shown in Figure 2. The lead drug (Zejula) is approved and commercialized in both the U.S. and EU. Since launched in April 2017, Zejula is the most prescribed PARP inhibitor (as a maintenance therapy for patients afflicted by ovarian cancer in the U.S., who demonstrated the complete or partial responses to platinum-based chemotherapy). Moreover, the EU launch of niraparib (Zejula) continues in Germany. Zejula sales are improving drastically to provide a meaningful revenues stream to power other pipeline innovation. Asides from Zejula, there is another commercialized molecule, rolapitant (Varubi) that is approved as a prevention of the delayed chemotherapy-induced nausea and vomiting."

Figure 2: Therapeutic pipeline (Source: Tesaro)

On Nov. 09, 2018, Tesaro presented the early results for its ongoing Phase 1 trials (AMBER and GARNET) that are studying TSR-022 and TSR-042 at SITC. It seems that the market is unimpressed with outcomes, as the stock tumbled over 18% during the day’s trading session. However, we strongly believe that the drop is unwarranted. It is likely a market “overreaction,” or a “knee-jerk” response. That said, it’s important to assess the data of all trials within their appropriate clinical context for a more comprehensive and accurate view.

As an ongoing Phase 1 study, AMBER investigates the efficacy and safety of TSR-022 (an anti-TIM3) and TSR-042 (an anti-PD-1) monoclonal antibodies in two groups (i.e. cohorts) of patients. Of note, these patients had prior anti-PD-1 treatment yet their tumors are still progressing. As follows, one group has the deadly non-small cell lung cancer (“NSCLC”) while the other cohort has advanced melanoma (a potentially lethal skin cancer).

Per trial design, the patients are dosed with TSR-042 500mg in combinations with either TSR-022 100mg or 300mg every 3 weeks. At the data cutoff, one in 14 patients with NSCLC responded at the TSR-022 100mg dose (i.e., a 9% partial response rate). Interestingly, the partial response rate improved to 15% (3/20 patients) at the higher dose (i.e., TSR-022 400mg). Therefore, the data indicates that there is a “dose-response” relationship which underlies therapeutic efficacy. In our view, it’s very likely that there will be a 33% response rate at the 900mg dose because we noticed that the addition of 200mg increment raised the response rate by 6%

That aside, it is worthwhile to note that patients who are PD-L1 positive have better response. In specific, 4 out of 12 evaluable patients with NSCLC and PD-L1 positive tumors responded with either the 100mg or 300mg TSR-022 dose. This signifies a 33% response at the low dose. Hence, it’s very likely that the response rate will increase to at least 50% at the high dosage for PD-L1 positive tumors.

In contrast to AMBER, the ongoing Phase 1 GARNET study assesses TSR-042 alone in patients suffering from advanced solid tumors, including endometrial cancer, and recurrent NSCLC. Notably, patients are dosed with TSR-042 500mg every 3 weeks. The data at SITC only entails patients with NSCLC because their dosing is completed. Of 47 patients, 15 people experienced partial responses and thereby represents a 32% rate. There was also a 29.8% stable disease rate (14/47 patients). More interestingly, the responses were durable for 9/15 patients (i.e., a 60% ongoing response rate)

Similar to AMBER, patients with PD-L1 expression responded better to the drug. As follows, the PD-L1 expression is measured by Tumor Proportion Score (“TPS”) with 50% or greater as a high expression and less than 50% is low. In specific, those with TPS <1% (i.e., almost no PD-L1 expression) posted a 15.8% overall response rate (“ORR”); whereas, the ORR is much higher at 38.5% for TPS 1-49%.

In addition, Tesaro presented the safety data for TSR-033 (an anti-LAG3 antibody) in patients with advanced solid tumors who are participating in the ongoing Phase 1 open-label study coined CITRINO. Accordingly, TSR-033 is well tolerated across different dosages. CITRINO is currently enrolling patients treated with TSR-033 in combinationS with TSR-042 500mg. Of note, both TSR-022 and TSR-042 also showed a favorable safety profile.

As earnings revealed many developments, we’ll assess the latest earnings report. For the third-quarter earnings that ended on Sept. 30, 2018, Tesaro posted $63.6M in revenues compared to $41.8M for the same period a year prior. This signifies a 52.1% year-over-year improvement. Nearly all revenues came from Zejula.

Additionally, there were $137.1M ($2.49 per share) net losses versus $25.3M ($0.47 per share) declines. This signifies a 429% worsening in the bottom line earnings. Nevertheless, investors should be cognizant that it is the norm for a relatively young bioscience company like Tesaro to incur significant losses for years prior to banking a net profit (due to the lengthy and low success rate of the innovation process). That aside, the research and development (R&D) for the respective periods came in at $94.2M and $73.4M, thus representing a 28% increase. We generally view an increase in R&D positively because the R&D money committed today - while reducing the net earnings - can turn into significant profits tomorrow.

Pertaining to the balance sheet, there were $476.8M cash and cash equivalents, thus entailing a 25.6% decrease from the $643.0M for the prior period. Again, the cash position is expected to be lower, as Tesaro is aggressively advancing its pipeline. Based on the $202.6M quarterly burn rate, there should be adequate cash to fund operations for the next two quarters prior to the need for additional financing. Be that as it may, it’s very likely that the company will execute a capital raise soon to strengthen its balance sheet.

Earnings aside, it is important for investors to keep tab on the ongoing corporate developments for you to know what to expect from your business. Therefore, we track the pertinent catalysts in Table 1 below. The most important event is the top-line reporting for PRIMA that is anticipated in late 2019. PRIMA is a Phase 3 study of Zejula for pushing the said drug into the 1st-line indication for ovarian cancer. We strongly believe that this crucial catalyst will enable Tesaro to ramp up niraparib revenues by multiple folds. This is because most of the blockbuster drugs are 1st-line medicine. Commenting on the recent developments, the CEO (Lonnie Moulder) enthused:

"In the third quarter, we launched several initiatives to grow the use of Zejula for recurrent ovarian cancer and we continued to execute on our development strategies focused on gynecologic and lung cancers as we approach a period of significant data readouts. Following results of the Phase 3 PRIMA trial next year, we intend for Zejula to benefit patients throughout all stages of their ovarian cancer journey, including First-line, recurrent, and late-line treatment settings. Our immuno-oncology pipeline continues to advance, led by our anti-PD-1 antibody, TSR-042, for which we are on track to submit a BLA next year. We look forward to initial data from the Phase 1 AMBER trial of our anti-TIM-3 antibody, TSR-022, in combination with TSR-042, which will be presented at SITC Annual Meeting next week."

Latest developments

Clinical

Results of GARNET were presented at ESMO with TSR-042 well-tolerated and demonstrated the encouraging efficacy for endometrial cancer.

The $18M milestone payment earned for the advancement of GALAHAD (a trial that studies niraparib in metastatic castration-resistant prostate cancer). This is also quite important to the future revenues increase for Zejula.

Other

Zejula revenues improved by 61% year over year. Zejula is now approved in 33 countries worldwide.

Zai Lab announced the Zejula approval in Hong Kong on Oct. 22, 2018.

Tesaro and actress Cobie Smulders launched, “Not on My Watch” to empowered the ovarian cancer community.

Outlook

The top-line results for PRIMA trial studying Zejula monotherapy as the 1st-line treatment for ovarian cancer are expected in late 2019.

TSR-042 BLA submission is projected for H2 2019.

Table 1: Catalyst summary (Source: Integrated BioSci Investing)

As the PRIMA endpoints are crucial to the future revenues increase, we’ll conduct a clinical forecasting for the aforesaid Phase 3 trial. Leveraging our Integrated BioSci framework of “molecule analysis” - that took into accounts different scoring variables, including available trial data (“TDV”), comparative molecular analysis (“CMV”), structural design (“SDV”), clinical trial setups (“TSV”), and disease specificity ("DSV") - we prognosticated that there are over 65% chances that Zejula will procure positive outcomes, thereby indicating a “more than favorable” reporting.

Notably, TDV and DSV factored substantially into this data forecast. The prior Zejula data is stellar to enable its approval as a maintenance therapy for ovarian cancer in 33 countries: it is the major determinant to PRIMA success. In other words, it is reasonable to expect the aforesaid drug to achieve similar findings in this trial.

Regarding qualitative analysis as shown in Table 2, Zejula scored a high rating on scientific novelty because a PPAR inhibitor is novel yet it is not as exotic as CAR-T or gene therapy. Nevertheless, we rated the unmet medical needs extremely high, because the death rate for advanced/resistant ovarian cancer is “off the roof.” This is one of the deadliest cancer. Taken altogether, there should be an extremely high ease of regulatory approval. Moreover, the stellar FDA Commissioner (Dr. Scott Gottlieb) lowered the regulatory hurdles to enable an unprecedented delivery of life-saving therapeutics to patients which should help out Zejula.

Qualitative analysis for Zejula

Scientific novelty (product differentiation) High

Unmet medical needs (therapeutic demand) Extremely high

Ease of regulatory approval Extremely high

Table 2: Qualitative metrics assessment (Source: Integrated BioSci Investing)

Warren Buffett stated that two excellent analysts can assess the same company and come up with distinct figures. Hence, one should take valuation within its appropriate context. To minimize subjectivity, we employed the comparative market analytical method (of gauging similar firms to give investors a rough estimate of an investment’s value). We usually check the Wall Street analysts consensus estimate to get the market sentiment on a particular stock. That said, Wall Street put the $56 price target (“PT”) on Tesaro.

In the next step, we’ll appraise Tesaro based on our estimated potential sales for Zejula (as the 1st line treatment for both ovarian and prostate cancers). And, we’ll take into account the 10 price to earnings (P/E) ratio, 54.9M shares outstanding, a 25% profit margin, and a 35% discount. Of note, we discounted this franchise by 35% due its chances of clinical and regulatory failure. The stellar Zejula quality and the large combined (prostate and ovarian cancers) market should yield the estimated potential revenues ranging from $1B to $2.5B.

Molecule and Potential Net earnings PT based on 54.9M PT after

franchise sales based on a shares outstanding 35%

25% margin and 10 P/E discounts Zejula in first

line ovarian $1B $250M $45.53 $29.59

cancer and

prostate cancer

Zejula in first

line ovarian $1.5B $375M $68.30 $44.39

cancer and

prostate cancer

Zejula in first prostate cancer

line ovarian $2B $500M $91.07 $59.19

cancer and

prostate cancer

prostate cancer

Zejula in first

line ovarian $2.5B $625 $113.84 $73.99

cancer and

prostate cancer

Table 3: Valuation analysis (Source: Integrated BioSci Investing)

In the final step, we averaged all PTs and thereby arrived at $51.79. Our PT is slightly higher than Wall Street and represents a 106% upside from the $25.10 current market quotation. The actual PT can be higher due to the various molecules in development: our valuation is solely based on the flagship molecule, Zejula.

For a small bioscience firm, the primary risk is whether the lead molecule will pass its clinical trials. If the drug fails to post positive data, the stock can tumble over 50%. Conversely, if the data reporting is positive, investors can expect the stock to be catapulted to the new high by similar (or greater) magnitudes. The aforesaid risks are less applicable to Tesaro because Zejula is already approved worldwide. As a result, we believe that the most important concern is if the firm can successfully push Zejula into the 1st-line treatment for ovarian as well as prostate cancer. There is a 35% chance of failure for the aforementioned binary event. Nevertheless, if other molecules fail to procure positive clinical outcomes, we can expect Tesaro to tumble by 15% and vice versa. Even if the aforesaid medicines will be approved, they might not generate substantial sales due to market competition and other unforeseen variables.

In all, we raised our recommendation on Tesaro from a speculative buy to a buy. We also increased our rating from three to four stars. And, we augmented our (two to three years) PT from $50 to $51.79 to be most representative of our valuation. Tesaro is powered by a superb approved-drug, Zejula that is scientifically and clinically validated. It is already being used as a maintenance therapy for ovarian cancers yet the company is increasing its launch efforts. Even better is that Tesaro is pushing Zejula into a 1st-line drug for ovarian cancer that, in and of itself, will unlock the most value for the company. That aside, Zejula is being advanced as a drug for metastatic prostate cancer which has a huge market. Our research on another company, Clovis Oncology (NASDAQ:CLVS) demonstrated that PPAR inhibition can be an excellent approach to treating prostate cancer. Regarding the latest data for other pipeline medicines (TSR-022, -042, and -033), the early data are promising in our views. Nonetheless, the market usually expects “home run” results. Therefore, the recent share price depreciation indeed created an excellent entry point for investors wishing to get in this highly promising company.

About Integrated BioSci Investing

We’re honored that you visited us. Founded by Dr. Hung Tran, MD, MS, CNPR, IBI is uncovering big winners. For instance, Nektar, Spectrum, Madrigal, Atara, and Kite procured +94%, +69%, +127%, +138%, and +83%, respectively. Our secret sauce is extreme due diligence with expert data analysis. The service features daily research/consulting. While we publish some ideas publicly, those articles are available in advance and are discussed more extensively in IBI. We also reserve our best ideas exclusively for IBI members. And, we invite you to subscribe now to lock in the current price.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: As a medical doctor/market expert, Dr. Tran is not a registered investment advisor. Despite that we strive to provide the most accurate information, we neither guarantee the accuracy nor timeliness. Past performance does NOT guarantee future results. We reserve the right to make any investment decision for ourselves and our affiliates pertaining to any security without notification except where it is required by law. We are also NOT responsible for the action of our affiliates. The thesis that we presented may change anytime due to the changing nature of information itself. Investing in stocks and options can result in a loss of capital. The information presented should NOT be construed as recommendations to buy or sell any form of security. Our articles are best utilized as educational and informational materials to assist investors in your own due diligence process. That said, you are expected to perform your own due diligence and take responsibility for your action. You should also consult with your own financial advisor for specific guidance, as financial circumstances are individualized.