Message Board")

Single Share Trades - What's the Payoff?

May 11, 2021 18:44:43 GMT

lookingforatenbagger and highskier like this

Post by icemandios on May 11, 2021 18:44:43 GMT

Explanatory note: One must have access to Time and Sales datafeed which is typically available with Level 2 or TotalView applets.

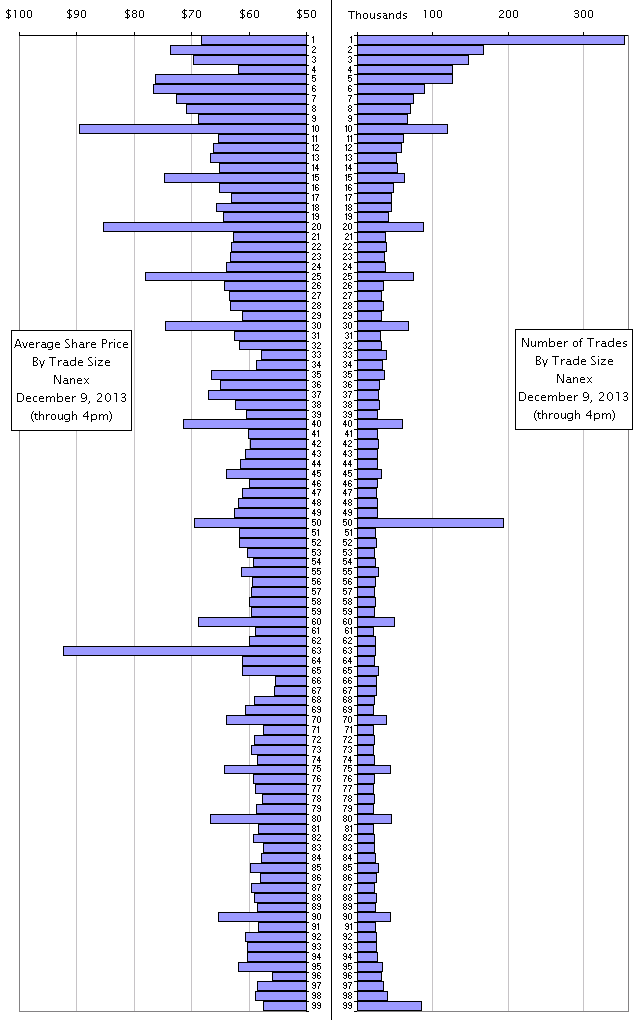

Nanex ~ 09-Dec-2013 ~ Odd Lots

On December 9, 2013, Odd lots (trades with sizes less than 100 shares) began reporting to the tape (Consolidated feeds). As of 4pm Eastern time, there were 4.5 million trades with sizes less than 100 shares, which is a whopping 17.4% of all trades. Before December 9, 2013, these odd lot trades were only reported in direct feeds. The average price of an odd lot trade in this sample was just $67 - it was expected to be a much higher number. The charts below break down the trade counts and average price by trade size, from 1 to 99 shares.

Link to chart

Link to chart

Excerpt from Themis Trading:

These charts raise some questions. Is there a direct relationship between a high incidence of odd-lot trades and exchanges that pay rebates? If so, why is that? If these odd lots were simply retail order flow, wouldn’t one expect to see a higher incidence on inverted exchanges, as those exchanges pay rebates to get taken, and surely order routers would be expected to take advantage of those rebates? Additionally, do odd lots result mostly from a resting round lot being hit by a an odd lot? Do odd lots result because resting orders start their lives as resting round lots, and get pinged into being an odd lot?

Could it be that this data infers that odd lots are not used predominantly by retail, but instead by high speed traders with some other purpose? What would that purpose be? Morgan Stanley recently published a note titled the Odd Lot Cascade Effect. Please reach out to your Morgan Stanley representative to get that note. The short note demonstrates that a resting round lot order (100 shares) which gets hit with a partial odd lot order (rendering the remaining resting order itself an odd lot), it loses price protection under Reg NMS. Could high speed traders be using small oddlots to degrade a resting front-of-the-queue round lot to a status where it is not protected by the NBBO, and therefore the orders behind it would benefit from a quasi-queue- jump if you will?

These are interesting questions. We hope the SEC looks at their data with a skeptical mindset; perhaps they can confirm such patterns, or others we have not been able to discern as of yet. The SEC then will potentially see how distortive the video game of rebate arbitrage actually is, where the collection of rebates has become so important to high speed traders, that they would willfully engage in games that deter real liquidity providers from ever displaying a public quote.

blog.themistrading.com/2013/12/odd-lots/

Nanex ~ 09-Dec-2013 ~ Odd Lots

On December 9, 2013, Odd lots (trades with sizes less than 100 shares) began reporting to the tape (Consolidated feeds). As of 4pm Eastern time, there were 4.5 million trades with sizes less than 100 shares, which is a whopping 17.4% of all trades. Before December 9, 2013, these odd lot trades were only reported in direct feeds. The average price of an odd lot trade in this sample was just $67 - it was expected to be a much higher number. The charts below break down the trade counts and average price by trade size, from 1 to 99 shares.

Link to chartExcerpt from Themis Trading:

These charts raise some questions. Is there a direct relationship between a high incidence of odd-lot trades and exchanges that pay rebates? If so, why is that? If these odd lots were simply retail order flow, wouldn’t one expect to see a higher incidence on inverted exchanges, as those exchanges pay rebates to get taken, and surely order routers would be expected to take advantage of those rebates? Additionally, do odd lots result mostly from a resting round lot being hit by a an odd lot? Do odd lots result because resting orders start their lives as resting round lots, and get pinged into being an odd lot?

Could it be that this data infers that odd lots are not used predominantly by retail, but instead by high speed traders with some other purpose? What would that purpose be? Morgan Stanley recently published a note titled the Odd Lot Cascade Effect. Please reach out to your Morgan Stanley representative to get that note. The short note demonstrates that a resting round lot order (100 shares) which gets hit with a partial odd lot order (rendering the remaining resting order itself an odd lot), it loses price protection under Reg NMS. Could high speed traders be using small oddlots to degrade a resting front-of-the-queue round lot to a status where it is not protected by the NBBO, and therefore the orders behind it would benefit from a quasi-queue- jump if you will?

These are interesting questions. We hope the SEC looks at their data with a skeptical mindset; perhaps they can confirm such patterns, or others we have not been able to discern as of yet. The SEC then will potentially see how distortive the video game of rebate arbitrage actually is, where the collection of rebates has become so important to high speed traders, that they would willfully engage in games that deter real liquidity providers from ever displaying a public quote.

blog.themistrading.com/2013/12/odd-lots/