Message Board")

ATRS SA Ready To Make Another Attempt @Breaking Out Above $5

Feb 4, 2021 13:37:36 GMT

icemandios, explorermadc, and 1 more like this

Post by tomsylver on Feb 4, 2021 13:37:36 GMT

Antares: Ready To Make Another Attempt At Breaking Out Above $5

Summary

* Company has solid momentum behind it on the back of solid gains in the proprietary portfolio.

* Nocdurna is expected to drive sales higher in 2021.

* Multiple growth drivers should result in significantly higher prices in 2021.

* Looking for a portfolio of ideas like this one? Members of Elevation Code get exclusive access to our model portfolio. Get started today »

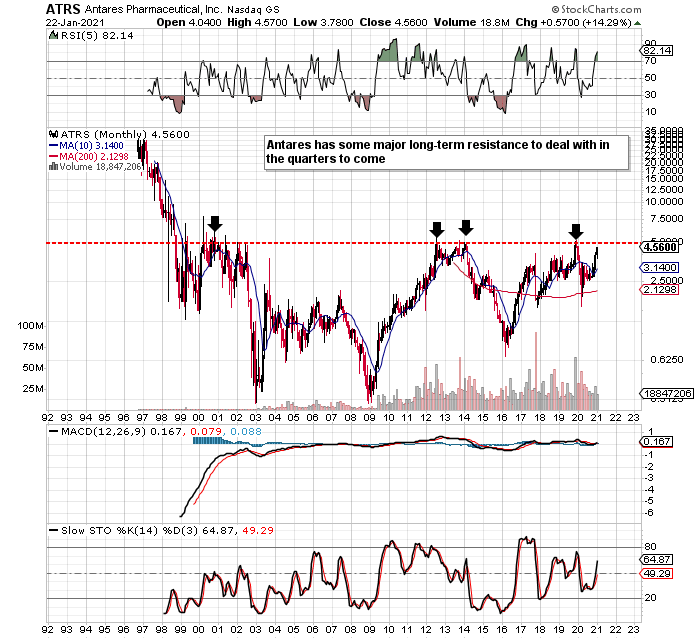

The last time we wrote about Antares Pharma (ATRS), we stated that plenty of long-term resistance existed on the long-term chart. Although the company finally broke well above this resistance level (Around the $3.50 level), there are plenty more battles to be won as we can see from the chart below. Technicians believe strongly that history repeats itself (which essentially means that stocks have memories) and we can see this clearly in the long-term chart of Antares at present.

In fact, shares first managed to struggle to clear the $5 level back in the year 2000. This pattern continued in 2012 as well as 2013 as well as the recent attempt in late 2019. With shares now trading at the $4.56 level, we fully expect another assault at that critical $5 level. Time will tell if shares will be able to break through early this year.

The technical chart definitely has ramifications for how we trade and invest. Why? Because the longer a trend has been in place (resistance at $5 for example), the harder it is for shares to develop a totally new trend. The flipside of this is that if Antares can see new ground for the first time in more than two decades, then that $5 level now becomes really strong support. Therefore let´s delve into some of the trends of the key financial metrics to see how much firepower the firm has at present with respect to its fundamentals.

The most recent third quarter definitely highlighted the strong momentum the firm is enjoying at present. Sales increased by 17% a year over a rolling year basis and by 24% sequentially to come in at $40 million for the quarter. Net profit came in at $5 million or $0.03 per share which again was a record for the company. Suffice it to say, this is bullish for ATRS as the firm has never had these types of tail-winds with respect to its sales and earnings in past times.

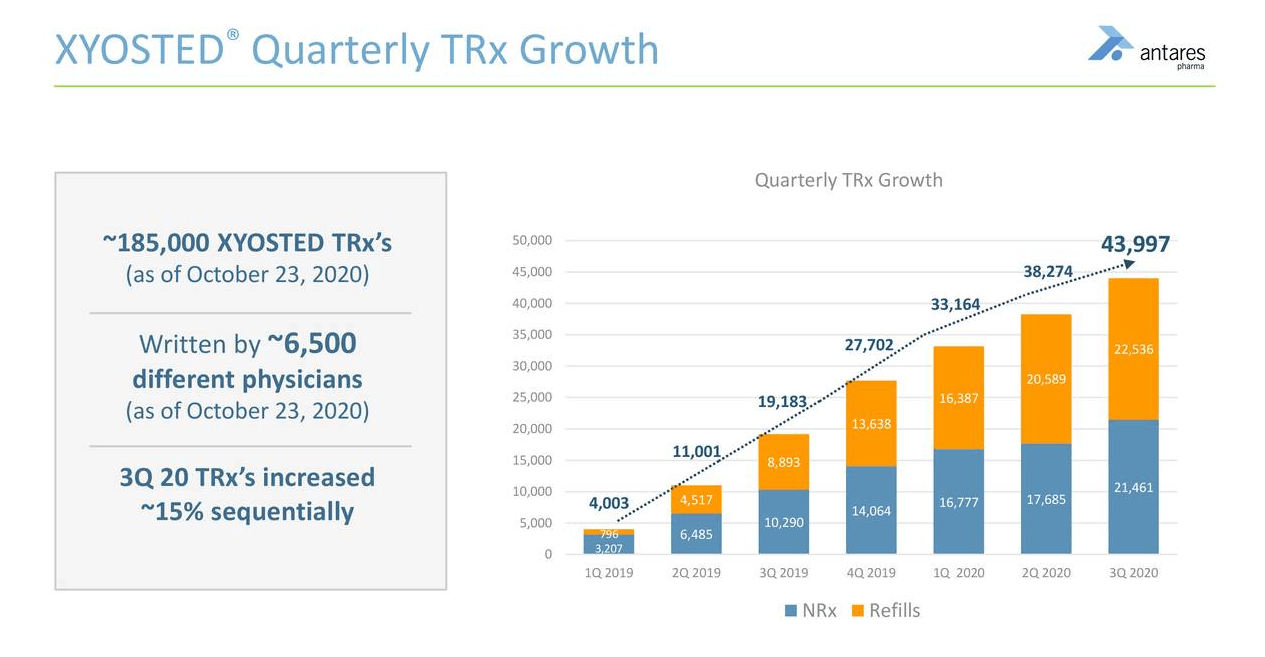

This momentum is expected to continue in the fourth quarter. Earnings are expected to come in at $0.04 per share on expected sales of $41.29 million. The advance is mainly coming from the strong top-line growth in the proprietary portfolio. XYOSTED & OTREXUP led the way bringing in almost $16 million of revenue in the quarter. XYOSTED is growing rapidly (as we can see below) and the fundamentals remain strong here due to a growing testosterone market and the fact that this this product can be administered at home.

Source: Company Presentation

The company is also bullish on NOCDURNA which is used to combat against regular trips to the bathroom at night. Antares recently announced an agreement with Ferring Pharmaceuticals in the US and this deal has resulted in the recently announced higher top-line guidance for 2021. Antares feels it will be able to piggyback on the success of XYOSTED with this rollout due to the significant number of relationships the sales force has built up. Management is expecting plenty of crossover with existing patients. Furthermore, because of how big this market potentially is (underdiagnosed), management feels that strong marketing will eventually lead to much higher demand here.

Next year, $0.24 is the bottom-line number predicted which means the forward earnings multiple looks far more attractive that the trailing one. However, from an assets and sales standpoint, there still exists a little bit of ambiguity as to how we should value this firm. Why? Well, the firm´s forward sales multiple looks pretty favourable as it comes in at 5.19 compared to the average in this sector which is 9.02. The company´s book multiple however (11.65) is more than twice the average in the sector at present. So, Antares has cheap sales (compared to the sector) but it has expensive assets. Assets though (P/B) are essentially what fuel sales and earnings growth over the long-term. This is why we see really strong profitability metrics in Antares at present especially in its ROE & ROA numbers because assets and equity tallies are very low compared to net profits for example.

So this would be our first risk in our opinion which would be some type of reversion to the mean with respect to the company´s assets. Plenty of spending will be needed in the quarters to come to build the business so it will be interesting to see if the growth curve can remain buoyant. With respect to XYOSTED for example, the question is how much growth the market is pricing in here in the quarters to come. To keep growth buoyant, the pace of refills is crucial which is why all focus must go into bringing new patients into the mix here.

Analysts who follow this company expect bottom-line earnings to rise by 260%+ next year. Obviously, if we get these types of numbers, there should be no issue with positive cash/flow like we have had over the first three quarters of 2020 ($14 million in operating cash/flow). The bigger the company gets though, the more risk that exists in execution. We state this because at the end of Q3, Antares had over $90 million of liabilities on the balance sheet which exceeded shareholder equity by over $25 million. Receivables for example have increased 4-fold over the past 10 quarters which means this line-item has outpaced sales growth by some margin. We would prefer more of a buffer here in the financials in case the pandemic was to take a turn for the worse for example.

Therefore, to sum up, there is a lot to like in Antares at present as it clearly has momentum on its side. Although the valuation may seem a tad lofty for value investors, the company is doing numbers which it never has done in the past. Although management state that there are plenty of growth drivers, we remain focused on the growth high margin proprietary segment. Let´s see how the firm can manage its risks going forward.

----------------------

Elevation Code's blueprint is simple. To relentlessly be on the hunt for attractive setups through value plays, swing plays or volatility plays. Trading a wide range of strategies gives us massive diversification, which is key. We started with $100k. The portfolio will not stop until it reaches $1 million.

Join Us here

-----------------------

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Jan. 25, 2021 2:44 PM ET

* Company has solid momentum behind it on the back of solid gains in the proprietary portfolio.

* Nocdurna is expected to drive sales higher in 2021.

* Multiple growth drivers should result in significantly higher prices in 2021.

* Looking for a portfolio of ideas like this one? Members of Elevation Code get exclusive access to our model portfolio. Get started today »

The last time we wrote about Antares Pharma (ATRS), we stated that plenty of long-term resistance existed on the long-term chart. Although the company finally broke well above this resistance level (Around the $3.50 level), there are plenty more battles to be won as we can see from the chart below. Technicians believe strongly that history repeats itself (which essentially means that stocks have memories) and we can see this clearly in the long-term chart of Antares at present.

The technical chart definitely has ramifications for how we trade and invest. Why? Because the longer a trend has been in place (resistance at $5 for example), the harder it is for shares to develop a totally new trend. The flipside of this is that if Antares can see new ground for the first time in more than two decades, then that $5 level now becomes really strong support. Therefore let´s delve into some of the trends of the key financial metrics to see how much firepower the firm has at present with respect to its fundamentals.

The most recent third quarter definitely highlighted the strong momentum the firm is enjoying at present. Sales increased by 17% a year over a rolling year basis and by 24% sequentially to come in at $40 million for the quarter. Net profit came in at $5 million or $0.03 per share which again was a record for the company. Suffice it to say, this is bullish for ATRS as the firm has never had these types of tail-winds with respect to its sales and earnings in past times.

This momentum is expected to continue in the fourth quarter. Earnings are expected to come in at $0.04 per share on expected sales of $41.29 million. The advance is mainly coming from the strong top-line growth in the proprietary portfolio. XYOSTED & OTREXUP led the way bringing in almost $16 million of revenue in the quarter. XYOSTED is growing rapidly (as we can see below) and the fundamentals remain strong here due to a growing testosterone market and the fact that this this product can be administered at home.

The company is also bullish on NOCDURNA which is used to combat against regular trips to the bathroom at night. Antares recently announced an agreement with Ferring Pharmaceuticals in the US and this deal has resulted in the recently announced higher top-line guidance for 2021. Antares feels it will be able to piggyback on the success of XYOSTED with this rollout due to the significant number of relationships the sales force has built up. Management is expecting plenty of crossover with existing patients. Furthermore, because of how big this market potentially is (underdiagnosed), management feels that strong marketing will eventually lead to much higher demand here.

Next year, $0.24 is the bottom-line number predicted which means the forward earnings multiple looks far more attractive that the trailing one. However, from an assets and sales standpoint, there still exists a little bit of ambiguity as to how we should value this firm. Why? Well, the firm´s forward sales multiple looks pretty favourable as it comes in at 5.19 compared to the average in this sector which is 9.02. The company´s book multiple however (11.65) is more than twice the average in the sector at present. So, Antares has cheap sales (compared to the sector) but it has expensive assets. Assets though (P/B) are essentially what fuel sales and earnings growth over the long-term. This is why we see really strong profitability metrics in Antares at present especially in its ROE & ROA numbers because assets and equity tallies are very low compared to net profits for example.

So this would be our first risk in our opinion which would be some type of reversion to the mean with respect to the company´s assets. Plenty of spending will be needed in the quarters to come to build the business so it will be interesting to see if the growth curve can remain buoyant. With respect to XYOSTED for example, the question is how much growth the market is pricing in here in the quarters to come. To keep growth buoyant, the pace of refills is crucial which is why all focus must go into bringing new patients into the mix here.

Analysts who follow this company expect bottom-line earnings to rise by 260%+ next year. Obviously, if we get these types of numbers, there should be no issue with positive cash/flow like we have had over the first three quarters of 2020 ($14 million in operating cash/flow). The bigger the company gets though, the more risk that exists in execution. We state this because at the end of Q3, Antares had over $90 million of liabilities on the balance sheet which exceeded shareholder equity by over $25 million. Receivables for example have increased 4-fold over the past 10 quarters which means this line-item has outpaced sales growth by some margin. We would prefer more of a buffer here in the financials in case the pandemic was to take a turn for the worse for example.

Therefore, to sum up, there is a lot to like in Antares at present as it clearly has momentum on its side. Although the valuation may seem a tad lofty for value investors, the company is doing numbers which it never has done in the past. Although management state that there are plenty of growth drivers, we remain focused on the growth high margin proprietary segment. Let´s see how the firm can manage its risks going forward.

----------------------

Elevation Code's blueprint is simple. To relentlessly be on the hunt for attractive setups through value plays, swing plays or volatility plays. Trading a wide range of strategies gives us massive diversification, which is key. We started with $100k. The portfolio will not stop until it reaches $1 million.

Join Us here

-----------------------

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.